An Investor's Guide to Syria's New Investment Framework

Licensing, incentives, obligations, and how Syria compares to its neighbors, a practical guide to Decision No. 1.

In November 2025, the Supreme Council for Economic Development issued Decision No. 1—the executive instructions for Syria’s investment law. If Decree 114 was the headline, Decision No. 1 is the fine print: 82 articles across 42 pages that detail how investment licenses are actually granted, what fiscal incentives attach to which sectors, how economic zones are established and governed, and what obligations investors carry once they’re in.

We published the first publicly available English translation of the decree alongside our earlier analysis of its key provisions. This piece does the same for the executive instructions. The full bilingual translation is available [here]. Below, we walk through the framework article by article—licensing mechanics, fiscal incentives, zone structures, investor rights and obligations, and dispute resolution—and flag the provisions that matter most for anyone evaluating an entry into Syria.

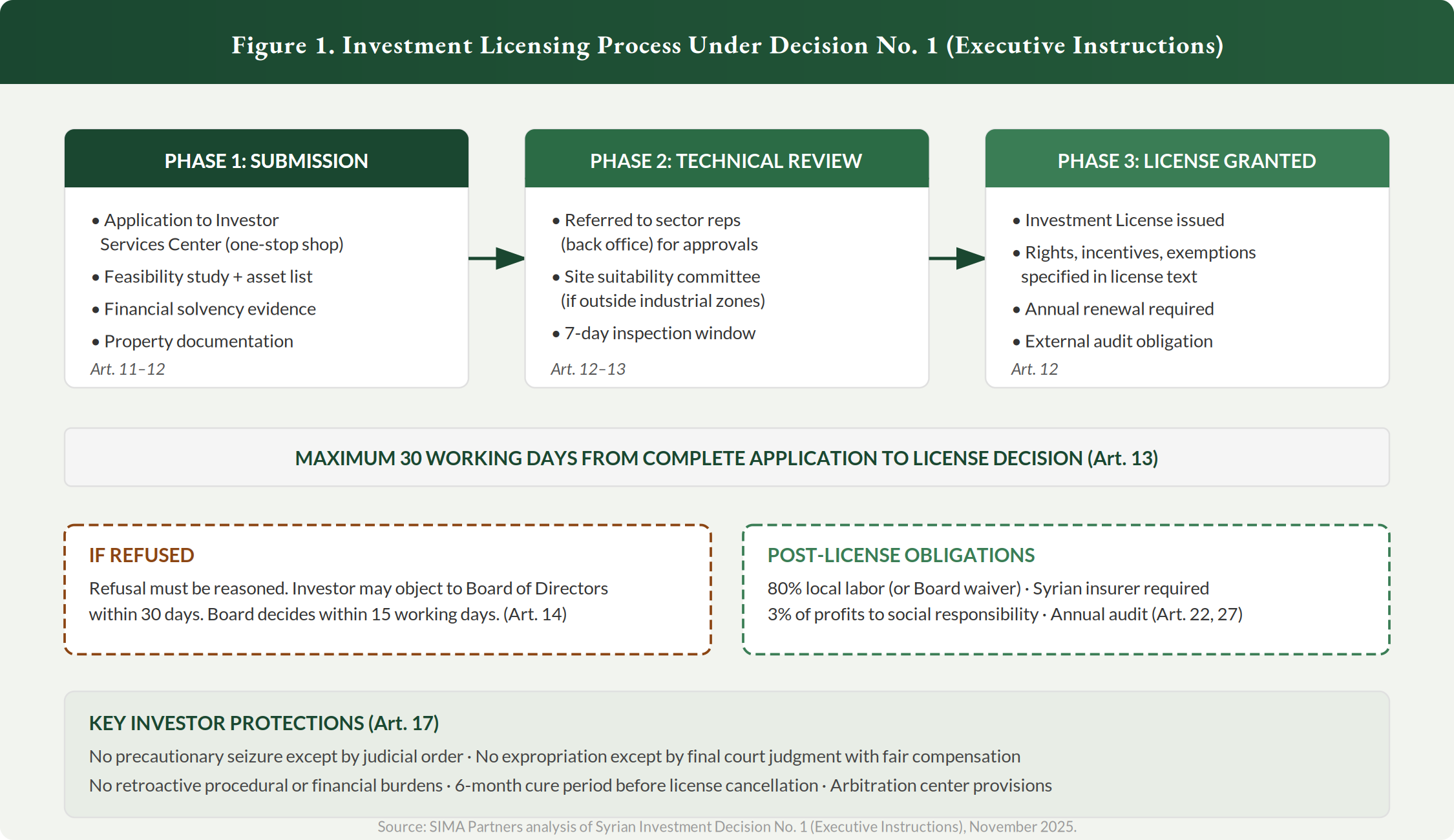

The Licensing Process: 30 Days, Three Phases

The executive instructions formalize a three-phase licensing process managed through the Syrian Investment Authority’s Investor Services Centers—one-stop shops where representatives from all relevant ministries sit under a single roof with delegated authority to issue approvals.

The process starts with an application to the Center, accompanied by an economic feasibility study, an asset list, evidence of financial solvency, and property documentation. If the project falls outside existing industrial zones, a site-suitability committee—chaired by the local SIA branch director and including representatives from regional planning, geology, and the relevant sector ministry—must conduct a physical inspection within seven working days.

Once submitted, sector representatives conduct a technical review. After all approvals clear, the SIA issues the Investment License—which explicitly specifies the rights, incentives, and exemptions that attach to the project.

The law caps the entire process at 30 working days from complete application to license decision. If the license is denied, the refusal must be reasoned. The investor has 30 days to object to the Board of Directors, which must rule within 15 working days.

That timeline is ambitious. Whether the one-stop-shop model delivers in practice—particularly in governorates where institutional capacity is weakest—will be among the earliest tests of the framework’s credibility.

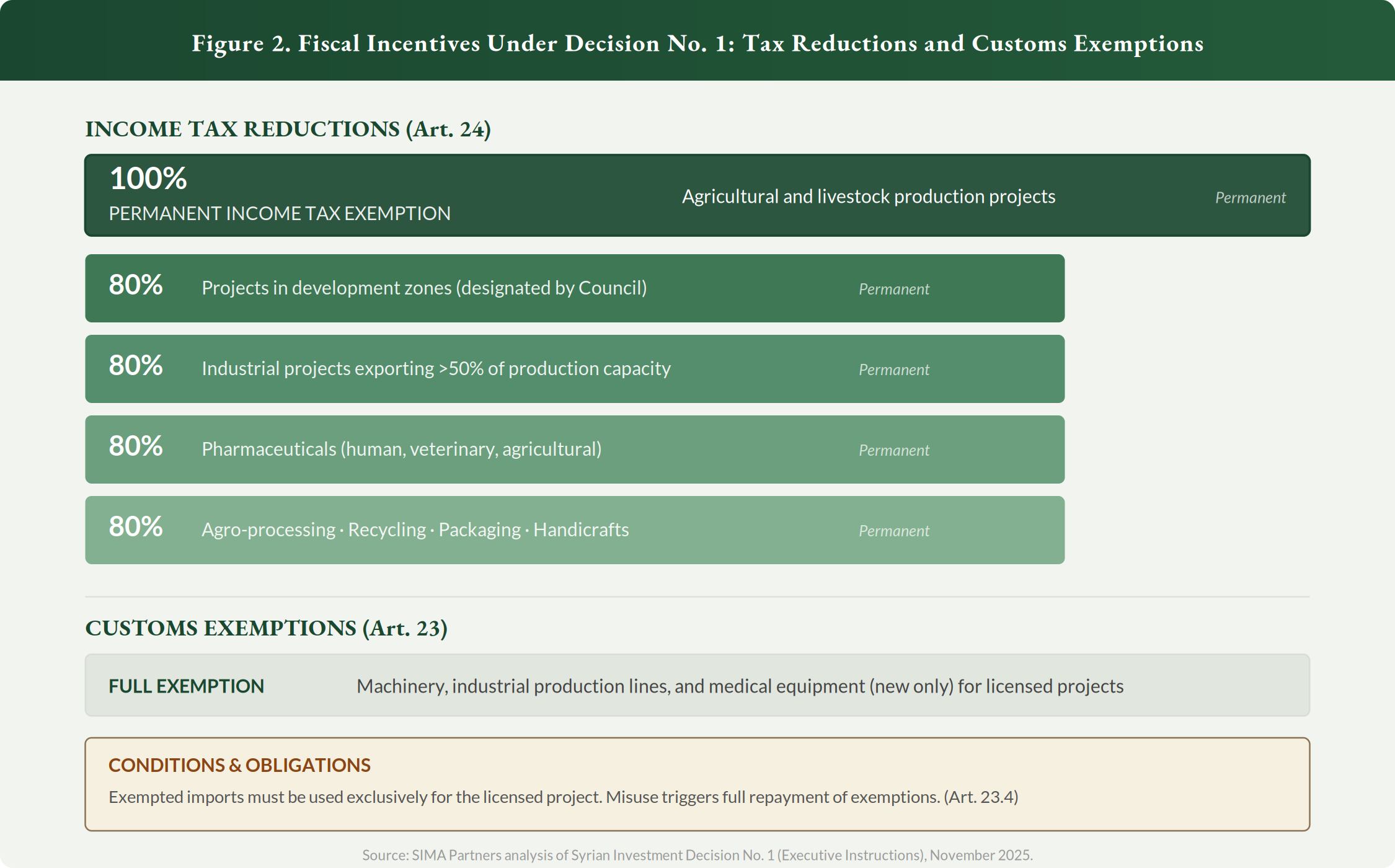

Fiscal Incentives: Permanent and Broad

The incentive structure carries over from Decree 114 and is now operationalized in detail. The headline remains the same: permanent tax exemptions with no sunset clause.

Agricultural and livestock projects receive a full, permanent exemption from income tax. Projects in designated development zones, export-oriented industrial projects (exporting more than 50% of capacity), pharmaceuticals, agro-processing, recycling, packaging, and handicraft facilities all receive a permanent 80% reduction.

On the customs side, machinery, industrial production lines, and new medical equipment imported for licensed projects are fully exempt from all customs duties and surcharges—provided they’re used exclusively for the project. Misuse triggers full repayment.

As we noted in our earlier analysis, the permanence of these exemptions is unusual even by post-conflict standards. Iraq’s 2006 investment law capped tax holidays at ten to fifteen years. Without sunset clauses, the risk is that first-movers lock in indefinite cost advantages, eroding the state’s long-term revenue base in the very sectors it’s trying to develop.

The executive instructions do not introduce any new time limits on these benefits. They do, however, add clarity on conditionality: exempted imports must be project-specific, and any breach of investor obligations can trigger cancellation of incentives and repayment of forgone duties.

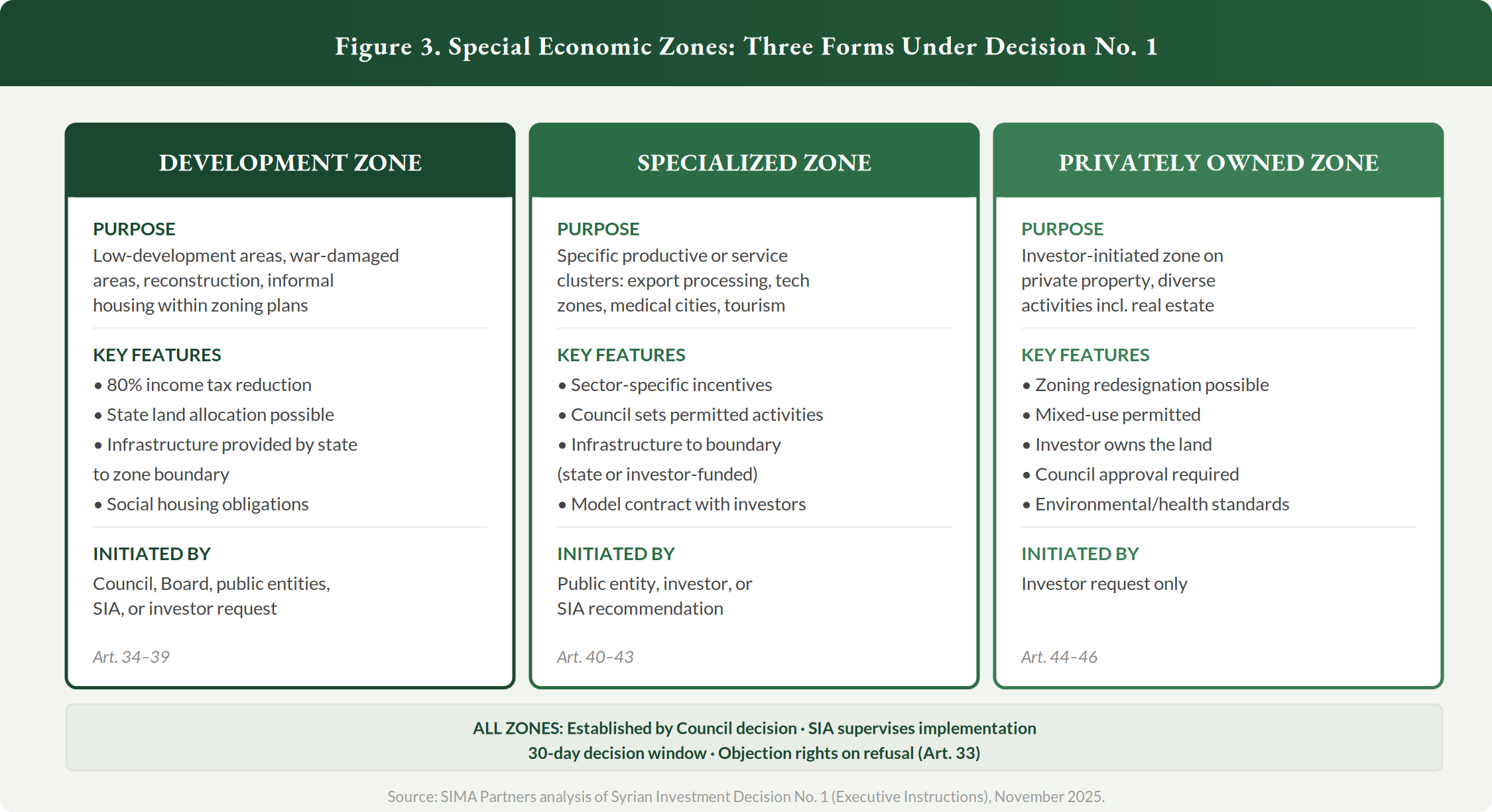

Economic Zones: Three Forms, One Council

The executive instructions introduce a detailed framework for special economic zones, dividing them into three forms—each with distinct governance, initiation mechanisms, and use cases.

Development Zones target war-damaged areas, underdeveloped governorates, informal housing, and reconstruction. They carry the 80% income tax reduction and allow allocation of state land. Infrastructure to the zone boundary is provided by the state. These can be initiated by the Council, public entities, the SIA, or investors.

Specialized Zones are designed for sector-specific clusters—export processing, technology, medical cities, tourism. They can be initiated by public entities, investors, or on SIA recommendation. The Council defines which activities are permitted and what incentives apply. Infrastructure is state- or investor-funded depending on the agreement.

Privately Owned Zones are investor-initiated, established on the investor’s own property. The Council can approve rezoning to match the project’s needs. These allow mixed-use activities including real estate development. The investor retains land ownership throughout.

All zones are established by Council decision, supervised by the SIA, and subject to a 30-day decision window. Refusals must be reasoned and are subject to objection.

The privately owned zone is a notable feature. It effectively allows an investor with a large enough land holding to request the creation of a self-contained economic zone—with Council-approved zoning changes and dedicated incentives. The model is permissive, and the degree to which it will be used by domestic versus foreign investors will be worth tracking.

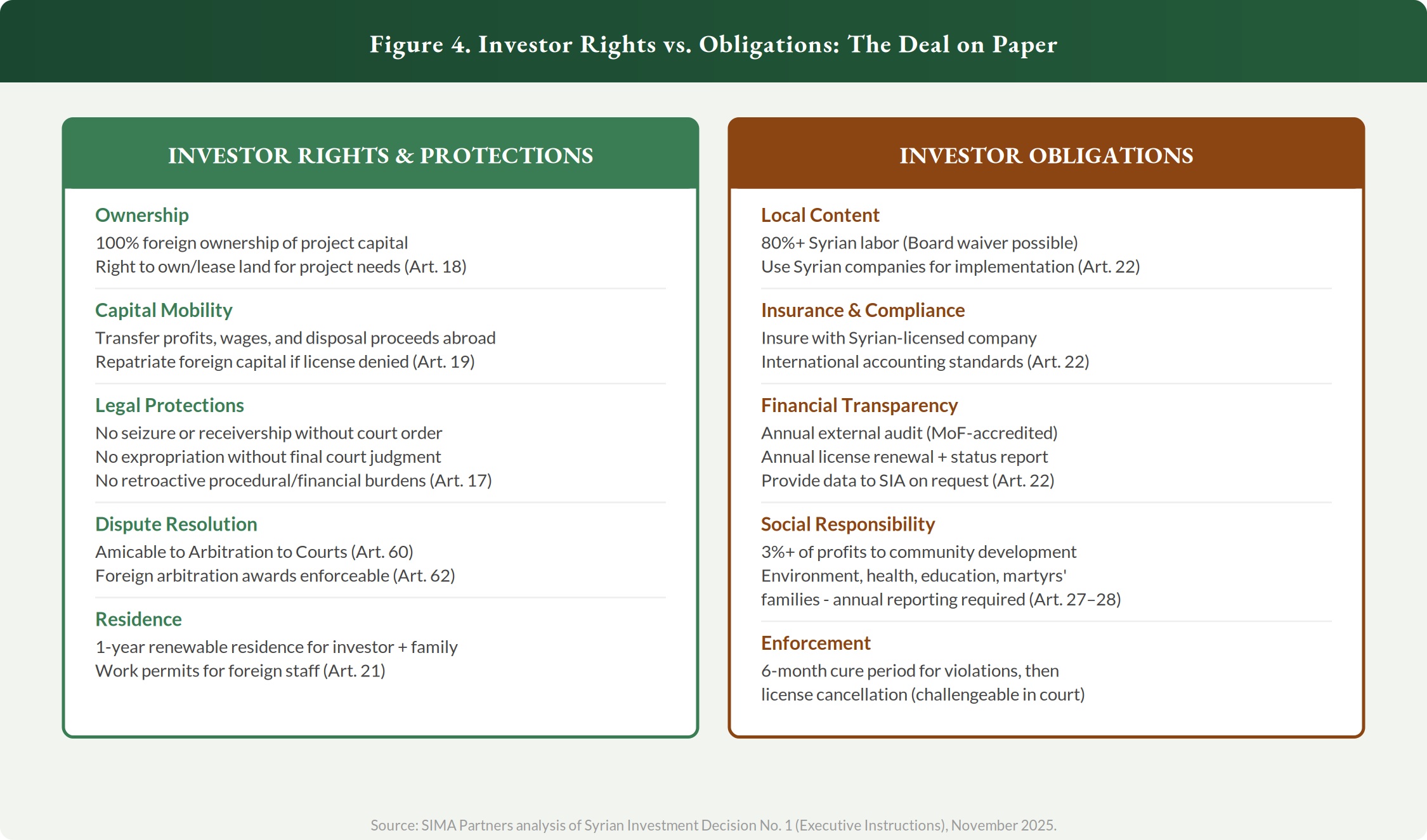

Rights and Obligations: The Full Ledger

The executive instructions flesh out the quid pro quo of the investment framework in granular detail. The investor gets broad protections and fiscal incentives; in return, the state imposes local-content requirements, transparency obligations, and a mandatory social-responsibility allocation.

On the rights side: 100% foreign ownership, the ability to transfer profits and wages abroad, one-year renewable residency, no precautionary seizure without a court order, no expropriation without a final judgment, and a prohibition on retroactive procedural or financial burdens. The dispute-resolution path runs from amicable settlement to arbitration (including foreign arbitration, whose awards are enforceable in Syria) to the courts—with investment lawsuits treated as urgent.

On the obligations side: at least 80% local labor (with a Board waiver for skill shortages), use of Syrian companies in project implementation, insurance through a Syrian-licensed company, international accounting standards, annual external audit, and annual license renewal. Projects must also allocate at least 3% of profits to community development—covering a defined list of social investments from environmental remediation to support for families of war casualties.

Two provisions stand out. First, the 3% social-responsibility allocation is not a suggestion—it’s a binding obligation with annual reporting requirements and SIA oversight. It effectively functions as an earmarked tax on profits, directed toward a range of social and environmental priorities.

Second, the 80% local labor requirement is among the highest in the region. Whether this is enforced rigidly or becomes a negotiation point for capital-intensive projects that require specialist foreign labor will shape the practical operating environment.

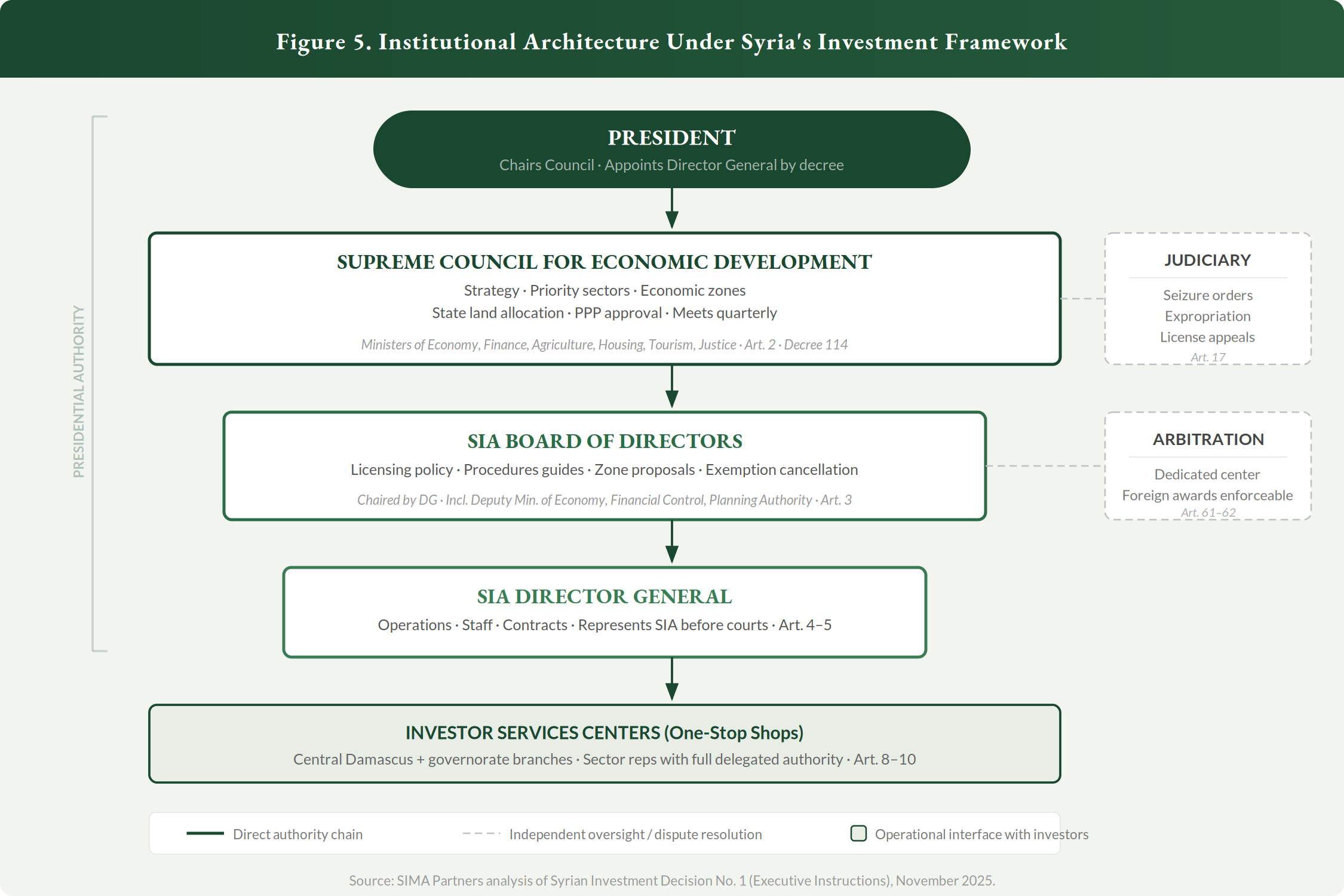

Institutional Architecture: Centralized by Design

The governance structure is vertically integrated and presidential.

The Supreme Council for Economic Development—chaired by the President—sets overall strategy, designates priority sectors, approves economic zones, allocates state land, and structures PPP frameworks. It meets quarterly and includes the ministers of economy, finance, agriculture, housing, tourism, and justice, among others.

Below the Council, the SIA Board of Directors manages licensing policy, procedures guides, and zone proposals. The Board is chaired by the Director General—who is appointed by presidential decree—and includes the Deputy Minister of Economy and Industry, representatives from the Central Agency for Financial Control, the Planning and Statistics Authority, the International Cooperation Authority, and two investor representatives.

The Investor Services Centers are the operational interface: one-stop shops in Damascus and governorate branches where sectoral representatives carry delegated authority to issue all permits and approvals.

The judiciary and an arbitration framework sit alongside this structure—at least on paper. The decree bars seizure, receivership, and expropriation without judicial orders, and provides for a dedicated investment arbitration center. But as we noted previously, whether these safeguards function as genuine constraints depends on the judiciary’s independence—which remains an open question.

The 3% Levy: Social Responsibility as a Profit Tax

One provision deserves closer attention. Article 27 requires all investors to allocate at least 3% of profits to community development. This is not a voluntary CSR program—it’s a binding obligation with annual reporting, SIA oversight, and a defined menu of eligible expenditures: environmental remediation, healthcare, vocational training, support for families of war casualties, afforestation, and renewable energy contributions, among others.

The funds flow into a dedicated account supervised by the Central Agency for Financial Control—not into the SIA’s own budget—and the expenditures are deductible from taxable profits. In effect, this functions as an earmarked tax on profits directed at social priorities chosen by the state.

No comparable mandatory allocation exists in Iraq, Jordan, or Egypt’s investment laws. Egypt allows voluntary CSR deductions of up to 10% of net income, but participation is optional. Syria’s version is compulsory. For investors modeling returns, the 3% should be treated as a line item, not a footnote.

Real Estate: The Sector That Will Absorb the Most Capital

The executive instructions devote significant space—Articles 47 through 52, plus the development zone provisions—to real estate development and investment. This is not incidental. With roughly 60% of Syria’s built environment damaged or destroyed and millions still displaced, housing and urban reconstruction will absorb more investment capital than any other sector in the near term.

The framework allows real estate developers to operate within development zones (with the 80% income tax reduction), on state land allocated by the Council, or on privately owned land rezoned with Council approval. Developers must be licensed by the SIA Board of Directors, and projects must allocate housing for low-income residents on facilitated terms. A 20% minimum completion threshold applies before any project can be transferred to a new developer.

For foreign investors, the path into Syrian real estate runs through the SIA. State-land allocation terms, zoning redesignation approvals, and the social-housing obligations embedded in the zone-establishment decisions will all shape project economics. The regulation governing state-land pricing—still unpublished—will be particularly consequential for this sector.

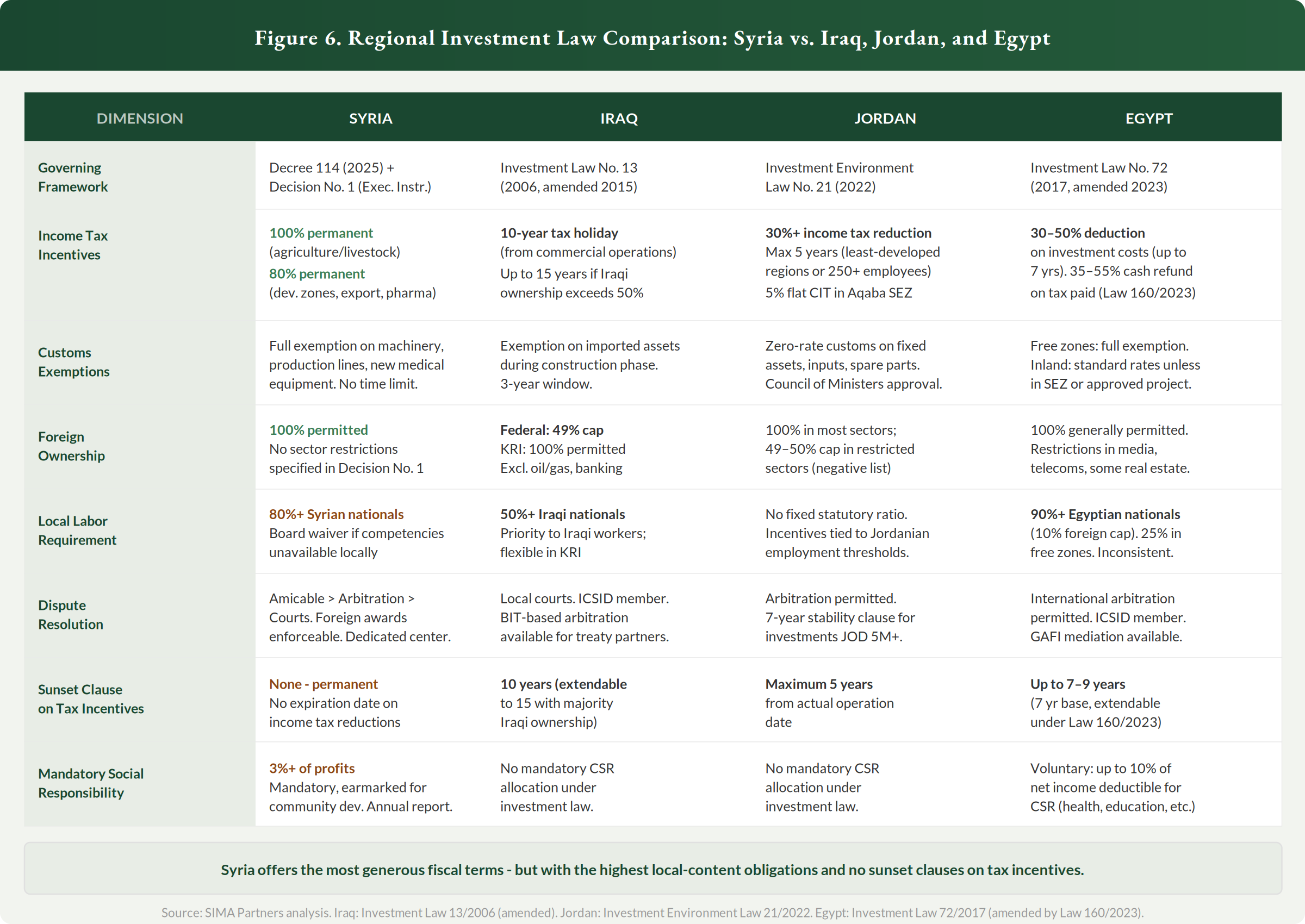

How Syria Compares: A Regional Benchmark

Syria’s investment law did not develop in a vacuum. Iraq, Jordan, and Egypt each offer their own frameworks for attracting foreign capital, with varying levels of generosity, conditionality, and institutional maturity. The comparison is instructive.

Syria’s fiscal terms are, on paper, the most generous in the region. No other neighboring country offers permanent income tax reductions of 80–100% without a sunset clause. Iraq caps its tax holidays at 10 years (extendable to 15 with majority Iraqi ownership). Jordan limits income tax reductions to five years and ties them to employment thresholds. Egypt’s incentives—recently expanded under Law 160 of 2023—take the form of investment-cost deductions (capped at seven to nine years) and cash refunds on taxes paid, not outright exemptions.

On foreign ownership, Syria is equally permissive. Decision No. 1 places no sector-specific ownership caps, allowing 100% foreign ownership across the board. Federal Iraq caps foreign ownership at 49% (though the Kurdistan Region allows 100%). Jordan maintains a negative list restricting foreign participation in certain sectors to 49–50%. Egypt generally permits full foreign ownership, with carve-outs for media, telecoms, and some real estate categories.

The tradeoff is on obligations. Syria’s 80% local labor requirement is the highest in the group—well above Iraq’s 50% and Egypt’s 90% (which is widely acknowledged as inconsistently enforced). Jordan ties employment thresholds to incentive eligibility rather than imposing a blanket ratio. And Syria’s mandatory 3% social-responsibility levy has no equivalent in any of the three comparators.

The net picture: Syria is making the most aggressive bid for capital in the region, with the deepest incentives and fewest ownership restrictions—but also the heaviest obligations and the least institutional track record. For early-stage investors, the question is whether the fiscal generosity compensates for the execution risk. The answer will depend less on the law itself than on how the SIA, the one-stop shops, and the courts actually perform.

What the Instructions Don’t Address

The executive instructions operationalize Decree 114 competently. They provide clear procedural steps, define institutional roles, and codify investor protections alongside obligations. But several areas remain unresolved:

Procedures Guides. The instructions repeatedly reference sector-specific “Procedures Guides” that will detail licensing requirements, financial costs, and time limits for each investment sector. These guides—prepared by the SIA in coordination with relevant ministries—are the next layer of operational detail. Until they’re published, investors in specific sectors are operating with an incomplete picture.

State Land Allocation Rules. The Council may allocate state land to investors, but the regulation setting out the bases for allocation—criteria, pricing, priority schedules—has not yet been issued. Article 30 requires the Council to publish a separate regulation. For sectors where state land is central to the investment (real estate development, industrial zones), this is a gap.

Minimum Asset Thresholds. The Council is empowered to set minimum fixed-asset thresholds for projects by sector and by zone, but the instructions do not publish these figures. Smaller investors have no way to assess whether their project scale qualifies.

Electronic Systems. The instructions reference electronic filing and inter-agency linkage systems that do not yet exist. The one-stop-shop model depends on functional coordination between sectoral representatives; the degree to which that coordination is digital versus paper-based will affect speed.

Investment Map. Article 64 requires all public entities to provide the SIA with detailed maps of state properties available for investment. This map—which would be a significant resource for investors scanning for opportunities—has not yet been published.

The Bottom Line

Syria’s executive instructions are a serious attempt to build a functioning investment regime from the ground up. The framework is detailed, the fiscal incentives are the most aggressive in the region, and the investor protections are real on paper. But the permanent tax exemptions come with the highest local-content obligations of any neighboring country, a mandatory profit levy with no regional equivalent, and an institutional architecture that has never been tested.

For investors evaluating early entry, the key documents to watch next are the sector-specific Procedures Guides, the state-land allocation regulation, and—most importantly—the first wave of actual license decisions. The law’s credibility will be established or undermined by whether the 30-day licensing timeline holds, whether the one-stop shops function outside Damascus, and whether the arbitration and judicial safeguards prove meaningful when tested.

The gap between law and practice will be determined by implementation. SIMA Insights will continue to track how the licensing process performs, how economic zones are designated, and which investors are first through the door.

The full bilingual translation of Decision No. 1 (Executive Instructions) is available [here].