Syria's Banking Problem and How to Solve It

Primer for anyone who wants to understand why Syria's reconstruction could stall at the point of capital, not because capital is absent, but because the pipes that move it do not work yet.

First in a SIMA Insights series on the structural bottlenecks to Syria's reconstruction. Where the city series asks where capital should be deployed, this series asks what has to clear before capital can move at all.

The Problem in One Paragraph

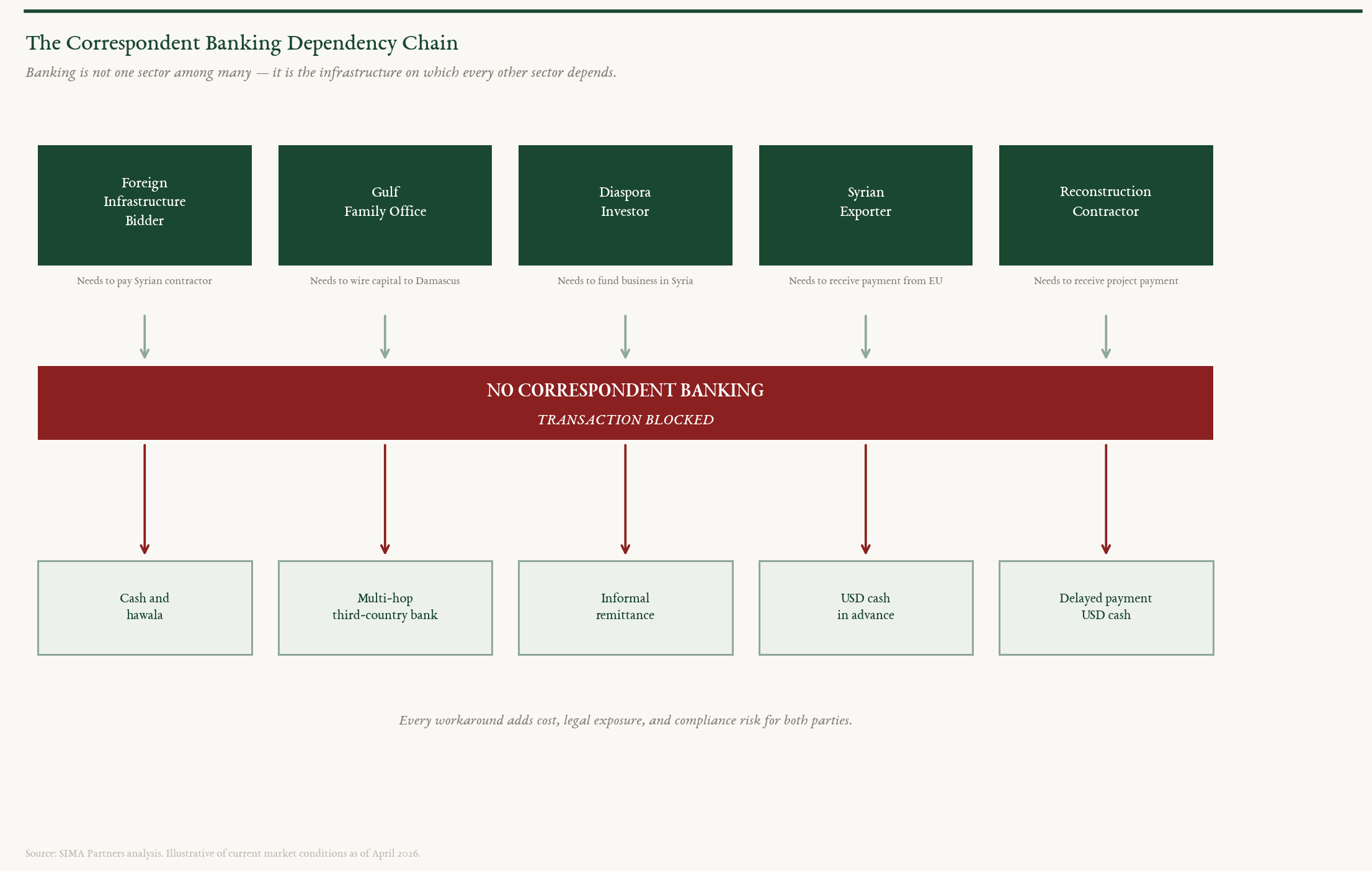

A foreign company wanting to pay a Syrian supplier, a diaspora investor trying to deploy capital in Damascus, a Syrian exporter waiting on a wire from a European buyer, and a reconstruction contractor expecting settlement on completed work all run into the same wall, which is that the banking system does not work for any of them. Sanctions have been lifted and the legal barriers are largely gone, and yet the $216 billion reconstruction opportunity that the World Bank has sized remains, for most practical purposes, inaccessible to the capital that would fund it. Almost every transaction connecting Syria to the global economy runs instead through cash, hawala, or expensive multi-hop workarounds that add cost and legal risk to every deal, and this is not a residual friction on the way to normalisation but the primary obstacle to Syria's economic recovery.

What Changed in 2025 and What Did Not

The pace of sanctions relief in 2025 was, by any historical standard, remarkable. The United States issued General Licence 25 in May, followed by an Executive Order on June 30 that revoked the six foundational Executive Orders comprising the Syria Sanctions Programme effective July 1. The EU lifted sectoral sanctions on energy, transport, and banking in February and May of that year, and followed in November with a FAQ clarifying that EU banks are now permitted to open accounts in Syria, establish correspondent banking relationships with Syrian institutions, and open branches. The United Kingdom similarly relaxed sectoral sanctions on banking and finance, while the Caesar Act’s secondary sanctions provisions were repealed through the National Defense Authorization Act in December 2025, and FinCEN issued exceptive relief permitting US financial institutions to open and maintain correspondent accounts for the Commercial Bank of Syria.

On paper, the architecture of isolation has been dismantled, but the banking system has not followed, and the reason is not legal but institutional, reputational, and structural. Global banks with US dollar clearing operations and exposure to US regulatory enforcement spent fourteen years systematically building Syria out of their risk frameworks, and they did not merely cease Syria-related activity but removed Syria from correspondent banking networks, trade finance platforms, compliance databases, and relationship management systems entirely. When sanctions were lifted, what those banks found was not a dormant relationship they could reactivate but an absence, a country that had been erased from their institutional memory, and rebuilding that memory requires due diligence, relationship development, regulatory comfort letters, and time that legislation alone cannot compress.

The State of Syrian Banks

Syria’s banking sector entered the post-Assad period in a condition that one analyst described in The National as a “black box,” because after fourteen years of isolation, sanctions, civil war, and economic collapse the sector’s internal state is largely unknown even to regulators, a problem Central Bank Governor Abdulkader Husrieh has acknowledged publicly. The sector underwent near-total collapse after 2011 as sanctions severed international relationships, economic decline destroyed the customer base, and the Syrian pound lost roughly 99 percent of its value, driving economic activity into cash and hawala networks that persist today and complicate any compliance assessment a foreign bank might attempt. A March 2025 US State Department report found Syria remained subject to significant money-laundering risks, citing ongoing conflict, the influence of non-state actors, and the absence of a functioning official banking sector.

Roughly fourteen private Syrian banks operated before the war, and their governance structures have not been publicly audited, their board compositions may include individuals on remaining SDN designations, and their capital adequacy ratios are unknown to external counterparties. The Commercial Bank of Syria has been cleared from the SDN list and is the subject of FinCEN’s exceptive relief, but Governor Husrieh stated publicly at a Middle East Institute event in Washington that the bank’s Federal Reserve account cannot be used for commercial activity because Syria remains designated as a State Sponsor of Terrorism, which is what Finance Minister Barnieh in Washington last week called the “last milestone,” the single remaining barrier without which everything else the Syrian government has achieved in the past year has limited practical value.

Washington, April 2026: Momentum Without a Timeline

The Syrian delegation to the IMF and World Bank Spring Meetings in Washington this month, led by Finance Minister Mohammed Yisr Barnieh and Central Bank Governor Abdulkader Husrieh, produced a dense schedule of high-level engagement. On April 14 the delegation chaired a technical roundtable of the Friends of Syria Group alongside World Bank Vice President Ousmane Diagana, with participation from Saudi Arabia, France, Germany, the United States, the United Kingdom, Italy, Switzerland, and the European Union. Over the course of the week they met with World Bank Managing Director of Operations Anna Bjerde, who accepted an invitation to visit Damascus, held discussions with Citibank on developing a government securities sector, and engaged the US Chamber of Commerce and representatives of major American companies across finance, energy, aviation, and technology.

Most significantly, on April 17 Minister Barnieh signed an agreement with the Qatar Fund for Development and Oliver Wyman, funded jointly by the Qatar Fund, the US Treasury, and the World Bank, to conduct a comprehensive assessment of Syria’s banking sector and produce a reform roadmap. A credible external assessment of the sector’s current state is a prerequisite for any international bank to begin the due diligence that correspondent relationship restoration requires, and the Oliver Wyman mandate is the first instrument capable of producing one.

What is absent from Washington, however, is a timeline. On the state sponsor of terrorism delisting, which is the single most consequential remaining barrier, Minister Barnieh told The National: “I’m optimistic that things will move in the right direction. How long? When? I’m not sure, but I hope to be very soon.” Equally absent is a structured interagency mechanism inside the Syrian government to drive banking reconnection with the urgency and coordination the problem demands.

Why Banking is Upstream of Everything

The banking problem is not one problem among several, because it sits upstream of every other reconstruction priority. A foreign infrastructure company can absorb political risk, navigate complex licensing, and manage construction in a post-conflict environment, but it cannot operate if it has no mechanism to move money through its normal treasury systems. A Gulf family office willing to deploy capital into Syrian real estate or manufacturing cannot execute that investment if wiring funds to a Syrian entity exposes it to regulatory risk in its home jurisdiction. A Syrian exporter who has secured a European buyer faces payment failure or multi-hop workarounds through third-country banks when the correspondent channel does not exist, and each hop adds days, fees, and legal complexity that erode the commercial case for the transaction.

The investor deterred by political risk is the exception, while the investor deterred by the inability to move money is the rule, which is to say that banking is not a sector in the conventional sense but the infrastructure on which every other sector’s viability depends.

The Overcompliance Problem

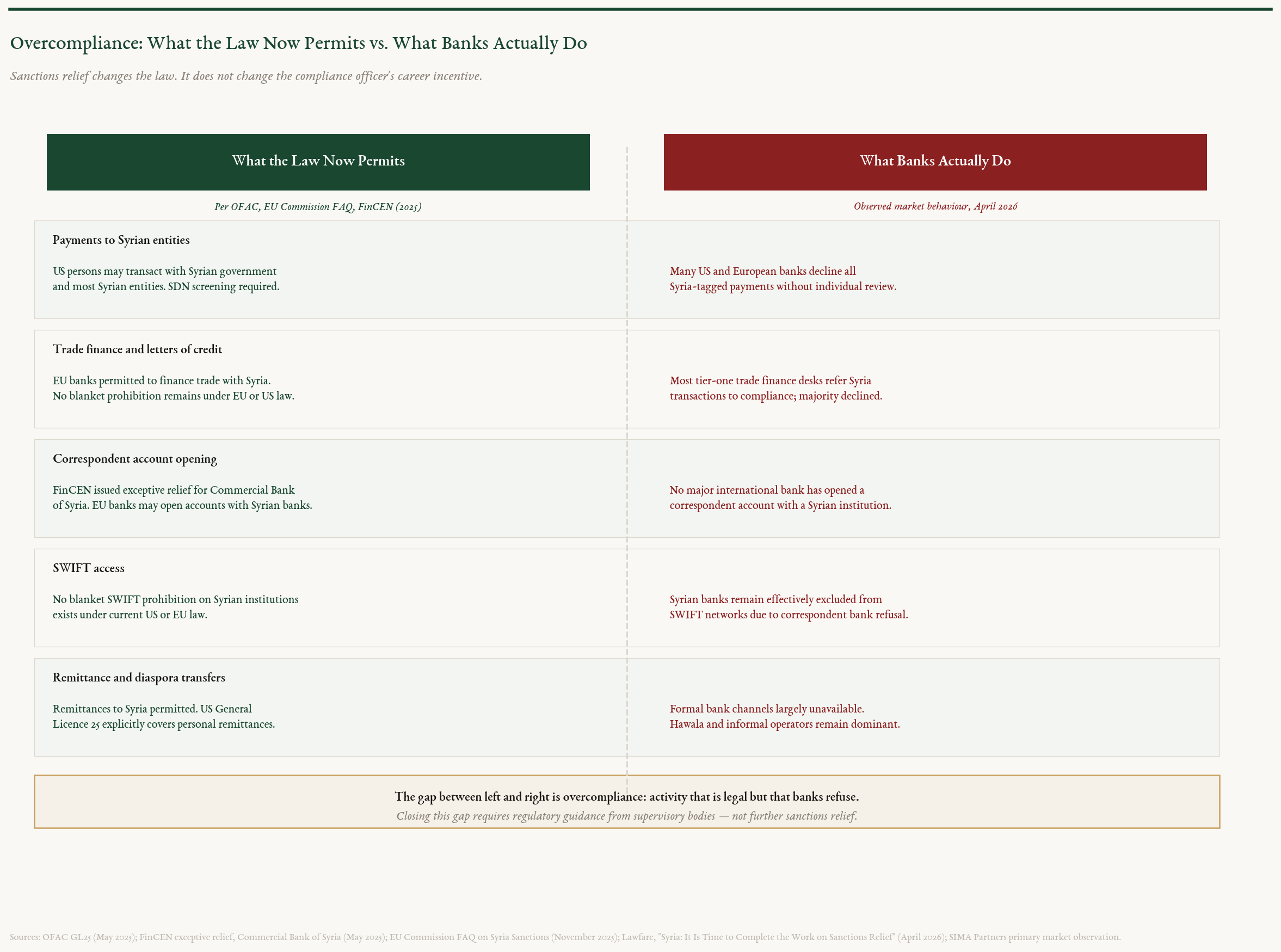

Overcompliance is the practice of banks restricting activity beyond what the law actually requires, refusing transactions, terminating relationships, or declining to open correspondent accounts not because doing so is prohibited but because the compliance cost and reputational risk of engaging exceed any conceivable commercial benefit. It is distinct from legal compliance, which follows the law, whereas overcompliance follows fear, and in Syria’s case fourteen years of maximum-risk designation trained the global banking system to treat any Syria-related transaction as presumptively prohibited, an institutional reflex that does not disappear when the legal designation changes. Addressing it requires a different intervention than lifting sanctions, because what is needed is for compliance officers at target banks to receive explicit regulatory guidance from their own supervisory authorities confirming that engagement is not only permitted but expected.

EU banks are now legally permitted to establish correspondent relationships with Syrian institutions, but legal permission and institutional willingness are not the same thing, and a legal opinion from a foreign ministry does not change the calculus of a compliance officer in Frankfurt or London. What changes that calculus is explicit regulatory guidance from their own supervisory authority, whether the ECB, BaFin, or the FCA, encouraging engagement and specifying the parameters of permissible activity. The European Commission’s November 2025 FAQ was a step in this direction, and more direct engagement with the ECB’s supervisory arm, the UK’s FCA, and the financial regulators of the UAE, Jordan, Turkey, and Saudi Arabia would accelerate the practical effect of a legal framework that already exists. The Syrian government’s foreign policy apparatus needs to engage not just with finance ministries and central banks in partner countries, but specifically with their financial regulatory bodies, requesting the guidance that gives supervised institutions explicit cover to act.

The FATF Problem

Syria has been on the FATF grey list since February 2010, placed there for strategic AML/CFT deficiencies and never removed, and FATF has been unable to conduct the required on-site verification visit, first because of the civil war and subsequently because of “security” concerns, which has left Syria in the unusual position of being grey-listed for sixteen years with the action plan’s actual implementation unverified on the ground. Every international bank conducting due diligence on a Syrian correspondent relationship must apply enhanced due diligence precisely because FATF has flagged Syria as a jurisdiction under increased monitoring, and grey-list status is therefore one of the most automatic and hardest-to-override triggers for bank refusal in the entire reconnection challenge.

Removal from the grey list would not by itself solve the correspondent banking problem, since the SST designation, the governance opacity of Syrian banks, and overcompliance all remain, but unlike SST delisting, which depends on US political decisions outside Syria’s control, grey-list removal depends almost entirely on actions Syria can take itself, namely facilitating the FATF on-site visit, demonstrating that the reforms committed to in 2010 have been implemented and sustained, and engaging actively with MENAFATF on the current framework. The Oliver Wyman assessment will produce the baseline diagnostic that FATF needs to conduct a credible on-site visit, but the assessment needs a publication commitment and a formal invitation to FATF before the October 2026 plenary, which is the most realistic near-term window for an on-site visit given FATF’s schedule. Grey-list removal is the one milestone in the entire banking reconnection agenda that Syria can drive on its own timeline, and it should be treated accordingly.

The Recommendation Framework

The problem has three layers, and any solution that addresses only one will fail. The legal layer is largely resolved, the regulatory layer (meaning supervisory guidance from partner-country financial regulators) is partially addressed and requires acceleration, and the institutional layer (meaning the rebuilding of Syrian banks into counterparties that international banks will actually accept) has barely begun. All three must run in parallel, driven by a single task force with presidential-level authority to break logjams across ministries.

Workstream 1 SST Delisting and FATF Grey List Exit: Both barriers belong in the same workstream because they share the same logic, which is that they are legal-layer stigmas that trigger automatic refusal by foreign banks regardless of the underlying commercial or compliance merits. SST delisting requires a sustained diplomatic campaign, meaning a dedicated team within the Ministry of Foreign Affairs working with diaspora lobbying networks in Washington, preparing a formal written submission to the State Department that documents Syria’s compliance with each statutory criterion, engaging registered lobbyists with direct experience on sanctions designation rescissions, and commissioning a legal opinion from a Washington firm on the specific procedural steps required. FATF grey list exit requires a different but equally urgent effort, because Syria has been on the grey list since 2010, completed its technical action plan by June 2014, and has never received the required on-site verification visit because of the security situation, which is a barrier that is now gone. A formal written invitation to FATF and MENAFATF requesting the on-site visit before the October 2026 plenary is the single most actionable step available, because it depends on no external political decision but only on Syria’s own initiative, and the Oliver Wyman assessment provides the baseline diagnostic the visit requires. Both SST and FATF are owned jointly by the Central Bank of Syria and the Ministry of Foreign Affairs and should be driven by a single integrated team with a single deadline.

Workstream 2 Regulatory Cover for Foreign Banks: Once published, the Oliver Wyman assessment gives foreign bank compliance officers something they currently lack, which is an externally validated, internationally credible document describing Syria’s banking sector and the reform programme underway. That document should be formally transmitted through central bank to central bank channels to the ECB, the UK’s Prudential Regulation Authority, the UAE Central Bank, the Saudi Arabian Monetary Authority, the Central Bank of Jordan, the Central Bank of Turkey, France’s ACPR, and Germany’s BaFin, with each transmission accompanied by a request for written regulatory guidance confirming that supervised institutions may establish correspondent relationships with compliant Syrian banks. The Central Bank of Syria should treat this as a bilateral regulatory diplomacy campaign, with a concrete target of receiving written guidance from at least three of these bodies within nine months of the Oliver Wyman assessment’s publication.

Workstream 3 Syrian Bank Governance Reform: No international bank will establish a correspondent relationship with a Syrian institution whose ownership structure, board composition, and capital adequacy are unknown, and while the Oliver Wyman assessment will establish the baseline, what follows must be a formal, public, time-bound governance review of every private Syrian bank seeking to participate in the reconnection programme, covering four questions: who owns the bank, whether any owners appear on remaining SDN designations, what the bank’s capital adequacy ratio is, and what its current AML/CFT framework looks like. Banks that pass receive a Central Bank of Syria certification, a public document a foreign correspondent can reference in its own due diligence file, banks that fail receive a defined remediation period, and banks that cannot remediate are consolidated or wound down.

The Task Force: A presidential banking reconnection team, co-chaired by the Central Bank Governor and the Finance Minister and with the Foreign Minister as the third member, reporting directly to the President monthly, is the institutional answer. The commission requires a full-time professional head with international banking experience, drawn from the diaspora if necessary, who is publicly accountable for delivery against milestones, and its mandate is fixed to a defined deadline, at the end of which it either declares success or presents an honest account of what was not achieved and why. Progress reports are published monthly in Arabic and English.

The Diaspora as an Operational Asset: Syrian diaspora professionals include compliance officers at tier-one banks, regulatory lawyers who advise central banks, lobbyists with State Department relationships, and bankers with direct correspondent banking experience at the institutions Syria needs to convince. The commission should establish a Diaspora Advisory Unit whose members are seconded to specific tasks within the three workstreams, because a compliance officer at a European bank who joins for six months to help draft the governance review criteria contributes more than a hundred diaspora members convened at a conference. The frame is operational participation, not symbolic representation.

The Urgency

The cost compounds monthly, because every month that correspondent banking remains absent is a month in which reconstruction capital allocates to other markets, foreign corporations defer Syria entry decisions pending resolution of the payment infrastructure question, Syrian exporters lose contracts to competitors with cleaner payment rails, and informal channels deepen their operational footprint. That last consequence is the most structurally damaging, because informal channels operating at scale do not merely substitute for the formal banking system but actively undermine the case for reconnection by demonstrating to international supervisory bodies that Syria’s economy is functional without it, and the longer informality persists as the operating norm, the lower the urgency to resolve the formal system and the harder it becomes to displace entrenched informal networks once formal channels do open.

The external environment Syria currently operates in is, by any reasonable assessment, the most permissive it has been in over a decade. The Friends of Syria Group has convened at the level of finance ministers and central bank governors, the Oliver Wyman assessment is now mandated and funded, the World Bank has committed a portfolio of $1 billion in grant-funded projects, Saudi Arabia and Qatar have made substantial diplomatic and financial investments in Syria’s re-engagement with multilateral institutions, and the US Treasury, the IMF, and the World Bank are actively engaged. This configuration of international support does not persist indefinitely, because it reflects a specific political moment that competing priorities, geopolitical shifts, and the natural attention cycle of international institutions will eventually erode.

The Syrian government has the remainder of 2026 and 2027 to convert this moment into durable institutional outcomes, meaning a formal SST submission on the table in Washington, a FATF on-site visit completed, written regulatory guidance issued by at least three major supervisory bodies, and the first correspondent banking relationships restored. Each of these is achievable within a short-term window, and none is achievable without a coordinated institutional mechanism that treats banking reconnection as the primary economic policy priority of the transitional period, which is what it is.

With contributions and review by Mansour Nehlawi, a former Citibank executive with banking and treasury experience across Asia, North America, and Europe, and a member of SIMA Partners’ Advisory Board.