Syria’s New Investment Law: An Aggressive Bid for Foreign Capital

Tax exemptions and centralized governance define Damascus’ strategy for increasing first-mover advantage.

Damascus alone does not have the capacity to finance an economic recovery. With a national reconstruction bill of $216 billion and a durably reduced tax base, the pace of Syria’s recovery will depend largely on how quickly foreign investment flows into the country.

President Ahmed al-Sharaa made the first major step in attracting that investment last June, issuing Syria’s first post-Assad investment law. We’ve published the first publicly available English translation of the decree, available here, alongside a detailed breakdown below of its key provisions and areas for improvement. In brief, the decree makes an ambitious bid for FDI by establishing a range of incentives for investors, even if the scale of its incentives may require reform to protect long-term competitiveness.

Executive-Led Development

The decree establishes two new institutions for the management of public wealth.

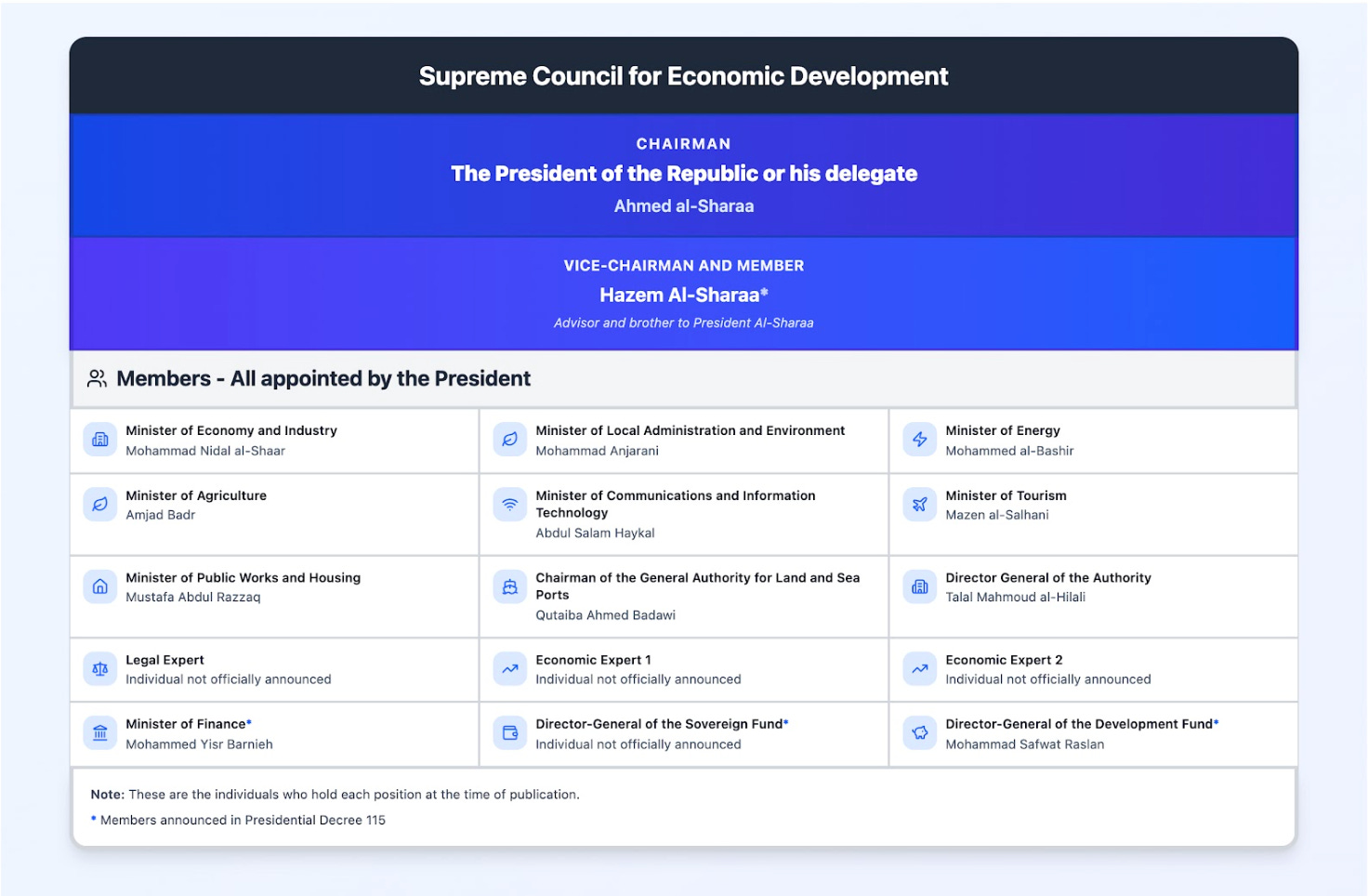

The Supreme Council for Economic Development is tasked with designing and implementing Syria’s overall economic strategy, identifying priority sectors, establishing investment zones, and structuring public–private partnerships. Chaired by the President or his delegate, reportedly vice-chaired by Hazem al-Sharaa, and populated by a number of ministers (see figure 1), the Council meets quarterly and operates under rules set by its Chairman.

The Council may allocate land from the state’s private property portfolio to investors, subject to regulatory guidelines, placing one of Syria’s most valuable economic assets—state-owned land—under centralized direction and granting the Council a significant role in capital allocation.

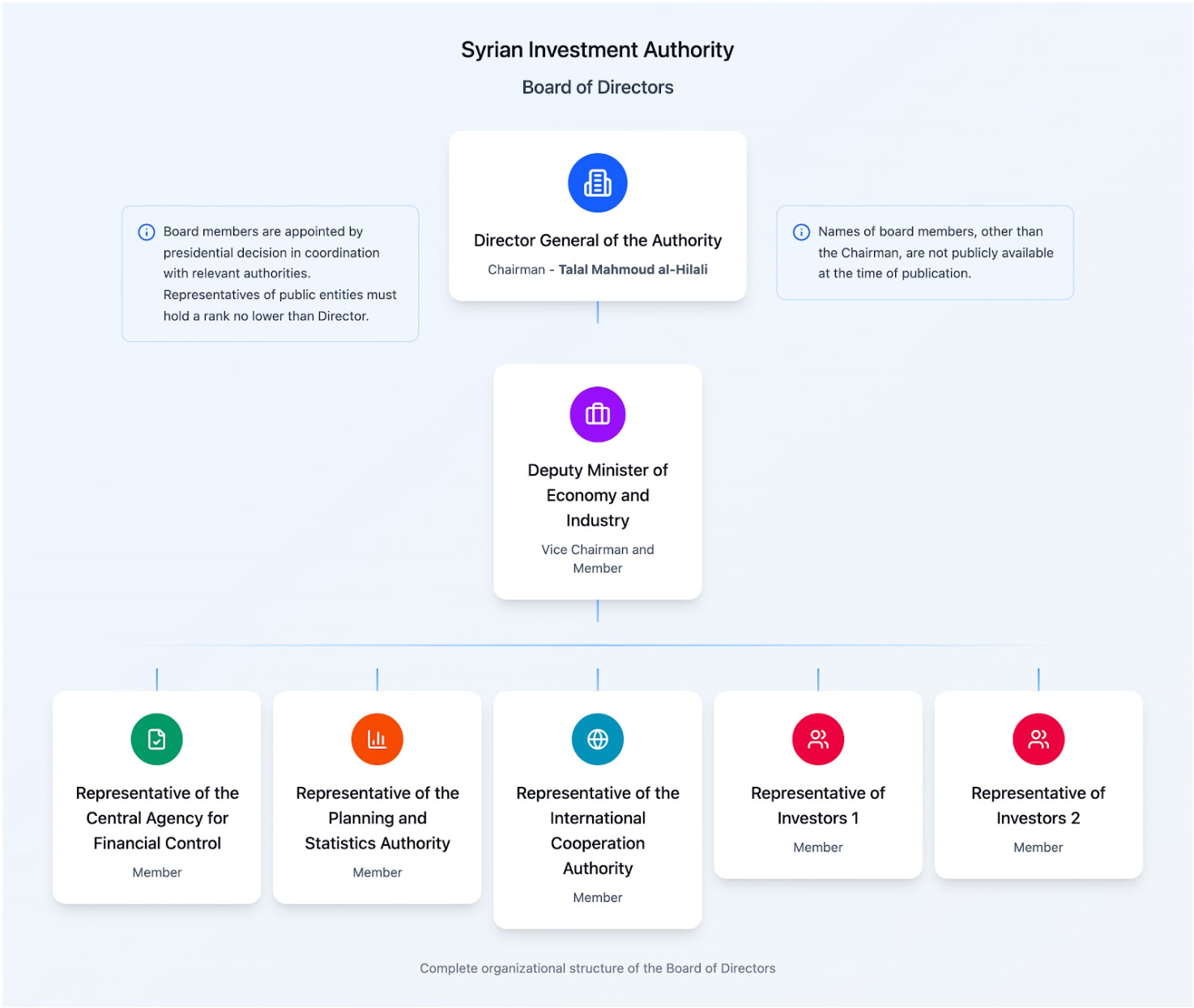

The second institution, the Syrian Investment Authority (SIA), functions as the investment law’s operating hand. It grants investment licenses, oversees compliance, and decides on investment applications. In addition, it operates Investor Service Centers, one-stop shops that bring representatives of relevant public entities under a single window. While the SIA is defined as having financial and administrative independence, it is explicitly affiliated with the president. Its Board of Directors is chaired by the Director General and includes the Deputy Minister of Economy and Industry, representatives of the Central Agency for Financial Control, the Planning and Statistics Authority, the International Cooperation Authority, and two investor representatives — all appointed by presidential decree. The Director General himself is appointed by decree and represents the Authority before courts and third parties.

For all its extension of presidential authority, the decree also empowers the courts. Projects may not be “subject to precautionary seizure or receivership,” nor to arbitrary license revocation, procedural burdens, or financial obligations, unless by reasoned judicial order. It also allows for the establishment of a specialized arbitration center for investment disputes. These provisions attempt to construct a formal dispute-resolution framework outside the executive, one aligned with international investment practice.

This shifts the locus of intervention from executive discretion to courts and arbitration centers, distancing itself from executive rule. That said, whether that safeguard proves meaningful depends on the judiciary's independence. Syria’s judicial system remains closely tied to the executive, where the president retains broad authority over judicial appointments and removals. While the decree places legal limits on executive interference, enforcement ultimately rests with institutions that are not yet fully autonomous.

Lowering the Cost of Entry

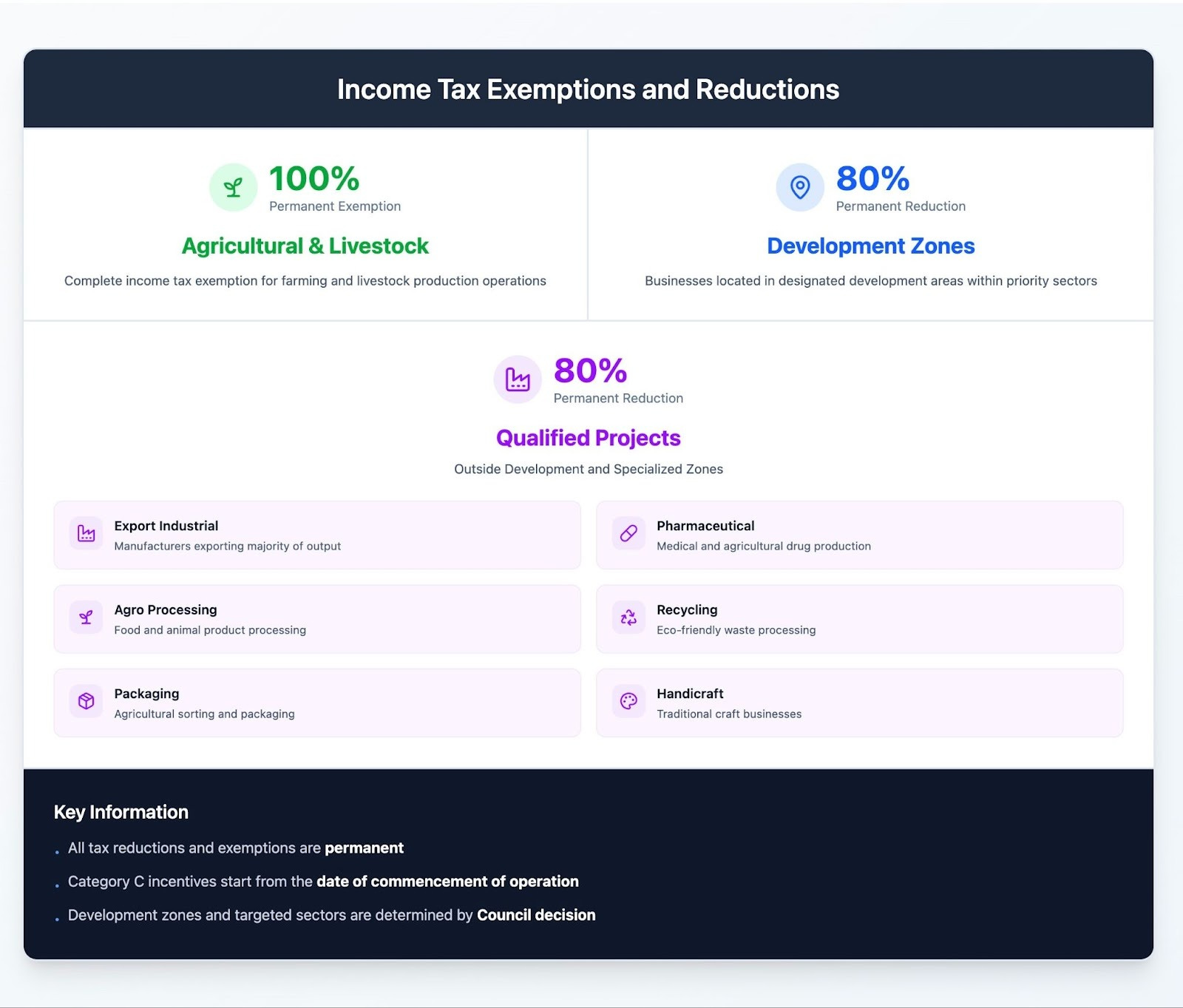

Reflecting the need to attract investment, the new investment regime features striking fiscal generosity. Agricultural and livestock projects receive a permanent 100% income tax exemption, while industrial projects exporting more than 50% of their production capacity, projects in development zones, pharmaceuticals, agricultural processing, recycling, packaging, and handicrafts will all receive an 80% reduction on income taxes (see figure 3).

Customs exemptions are equally broad, with imports of machinery, industrial production lines, and medical equipment necessary for licensed projects all exempted from customs duties and related surcharges.

Beyond sector-specific carve-outs, foreign investors as a class are granted significant advantages. They may own 100% of project capital, receive renewable one-year residence permits during both establishment and operation, and transfer full wages and profits abroad through Syrian banks. While those benefits do come with requirements to use Syrian companies in project implementation, employ at least 60% local labor, and insure projects through Syrian-licensed insurers, the law is generally quite favorable to foreign investors when compared with regional equivalents.

These pro-investor policies do come with tradeoffs. In the short term, aggressive incentives and centralized coordination may succeed in attracting capital during a period of extreme fragility. Over the longer term, permanent tax exemptions and concentrated authority could constrain fiscal capacity and limit domestic participation in key sectors.

Let’s take one feature: the absence of sunset clauses. Permanent tax exemptions are unusual in investment laws, even post-conflict ones. Iraq’s 2006 Investment Law, for example, capped tax exemptions at ten to fifteen years and limited customs benefits to three years. Absent sunset clauses, many of these sectors may become dominated by first-movers—early entrants whose investment bids are approved by the SIA under the current framework—that continue to enjoy tax exemptions indefinitely. Over time, these permanent incentives create cost asymmetries, locking in the competitive position of these firms and limiting the state’s ability to collect revenue from the largest companies in its priority sectors.

The result is a more aggressive bid for capital, but one that may constrain the state’s future fiscal capacity. In the immediate reconstruction phase, that tradeoff may appear justified. Over time, as the economy grows and public spending demands increase, the long-term erosion of the revenue base may become harder to defend. Whether the initial influx of capital justifies the long-term fiscal sacrifice is a question of political judgement, and one that merits wider debate.

The answer will also largely depend on the law’s implementation. In the months ahead, SIMA Insights will be tracking how bids are allocated to see who benefits most from the new framework. The distribution of investment licenses, the terms on which state land is allocated, and the credibility of arbitration and judicial safeguards will all determine will determine how attractive Syria becomes as a destination for FDI.