The Reconstruction Dividend: Aleppo

This is the first in a series examining the reconstruction potential of Syria’s cities, one at a time, through the same analytical lens.

There is a useful way to think about Aleppo, and it has nothing to do with sentiment or history or the human tragedy of the war, though all of those things are real and none of them should be minimised. The useful way to think about Aleppo, if you are trying to understand where Syria’s reconstruction capital should go, is as a machine that was dismantled and is now being reassembled, piece by piece, by the people who built it in the first place.

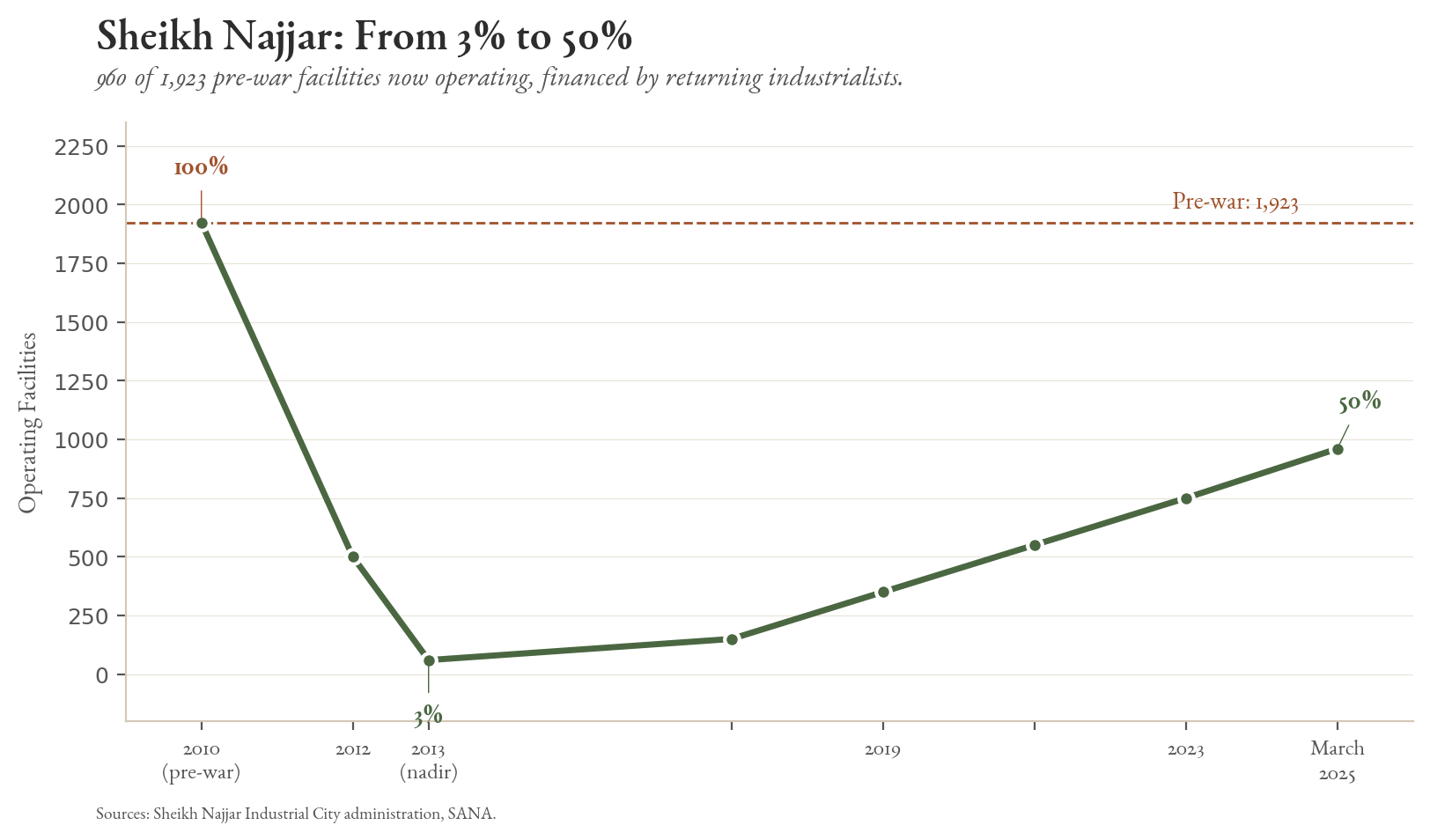

At its peak, the machine was formidable in both scale and sophistication, though not without structural weaknesses, including a wage share that was low and falling and a business environment shaped by political connections as much as by market forces. Aleppo’s governorate generated roughly a quarter of Syria’s GDP, approximately $15 billion in a $60 billion economy, and its industrial zones produced half of all Syrian manufactured exports, giving a single city greater manufacturing weight than many sovereign economies in the region. The textile sector alone accounted for a third of national industrial output, built and controlled by multi-generational industrial families whose knowledge, relationships, and capital defined the sector. A pharmaceutical cluster of roughly 70 privately owned plants covered 80% of Syria’s domestic drug consumption. The Sheikh Najjar industrial city, occupying 4,412 hectares northeast of the urban centre and ranking among the largest industrial zones in the Middle East, hosted 1,923 companies with over $3.4 billion in total investment by 2010, of which 40% were Turkish-owned and operating under a 2004 free trade agreement that had begun to weave Gaziantep and Aleppo into a single cross-border production corridor.

This was not an economy that happened to be located in Aleppo but rather an economy that could only exist in Aleppo, positioned at the junction of the Mediterranean, Anatolia, and the Euphrates plain, 50 kilometres from the Turkish border, equidistant from the sea and the river, sitting on trade routes that had been in continuous use since the Amorite kingdom of Yamhad four thousand years ago. Geography is not a metaphor here but a competitive advantage that survived the Mongol sack of 1260, the Timurid destruction of 1400, the Ottoman incorporation of 1516, and the double amputation inflicted by the redrawing of borders after the First World War, when the Treaty of Lausanne severed Aleppo from its northern hinterland and then France ceded the port of Iskenderun to Turkey in 1939, stripping the city of both its Anatolian trading partners and its Mediterranean outlet in a single generation and forcing its commerce to reroute through Latakia, two hundred kilometres to the southwest. The city rebuilt every time because its location made not rebuilding irrational, and the redirection of the Syrian capital from Aleppo to Damascus only reinforced the pattern: political demotion did not diminish commercial gravity. Neither did decades of neglect by successive Damascus-based governments, which systematically directed state investment, military infrastructure, and political patronage toward the capital and the coastal heartland while leaving Aleppo to generate a quarter of national GDP on the strength of its private sector alone, receiving a fraction of the public spending that its economic contribution warranted.

The commercial record bears this out: Aleppo hosted the first European consulates in the Levant (Venice in 1548, France in 1562, England in 1583), served as the headquarters of the Levant Company of London from 1581 until the late eighteenth century and was so central to the flow of goods between East and West that when Dutch competition disrupted Aleppo’s spice trade in the 1590s, the resulting loss of revenue was one of the triggers that prompted English merchants to found the East India Company in 1600, which would become one of the largest and most powerful commercial enterprises in history, conceived in part as a way to bypass the Levantine trade routes that Aleppo had dominated for centuries. In 1841 the city became the birthplace of Safra Frères & Cie., the banking house founded by the Safra family that would grow into the J. Safra Group, a conglomerate managing over $345 billion in assets globally today, and established one of the first commercial tribunals in the Ottoman Empire around 1855. The Baron Hotel, built by the Mazloumian family in 1909 as one of the first modern hotels in the region, hosted heads of state, diplomats, and literary figures from across the world, and the street on which it stands was renamed after it by the Syrian government upon independence. These are not antiquarian details but evidence of a pattern: international capital has been drawn to Aleppo for five centuries, and the question that shapes every investment decision today is whether the conditions exist for that pattern to reassert itself after the worst destruction of all.

What Was Lost

The war reached Aleppo in mid-2012 and did not relent for four years, dividing the city along a line of control that ran through its historic centre, with the government holding the west and rebel forces holding the east, and both sides subjecting the other to sustained bombardment that produced what was arguably the most concentrated episode of urban destruction since the Second World War. The population fell from 3.1 million to approximately 600,000 between 2010 and 2014, an 80% collapse that is difficult to find a modern parallel for, and the Aleppo Chamber of Industry estimated the cost at $55 billion in total industrial losses across the city’s industrial zones, with 85% of factories at Leyramun completely destroyed and only 200 of 1,326 enterprises at al-Kalasseh managing to resume by 2017. UNESCO assessed that roughly 70% of the Ancient City’s core zone had been affected to a degree that invited comparison with post-war Warsaw, and the February 2023 earthquake then compounded these losses by inflicting further structural damage across the governorate.

But the figure that matters most for investors appears in no damage report, because it is the human capital that left the city and has not returned. Aleppo’s industrial dynasties relocated and rebuilt: the Sabbagh Sharabati family established a $200 million textile complex in Egypt’s Sadat City and a second production facility in Turkey’s Kadirli, now producing 80 million running metres of denim annually with over 3,000 employees, while other Aleppine manufacturers clustered in Gaziantep’s organised industrial zones, and the city’s pharmaceutical chemists and engineers scattered from Amman to the Gulf. One textile industrialist, speaking to The National, described his departure as “not a commercial choice but a decision of survival” before going on to establish several firms around Bursa, and whether he and the thousands of skilled professionals like him choose to return will determine Aleppo’s economic trajectory more decisively than any infrastructure programme. The two million people who stayed through the war, who kept the city’s markets and workshops functioning on generator power and improvised supply chains, are the foundation on which any reconstruction rests, and any investor who fails to account for their experience and expectations will misread the market.

What Changed

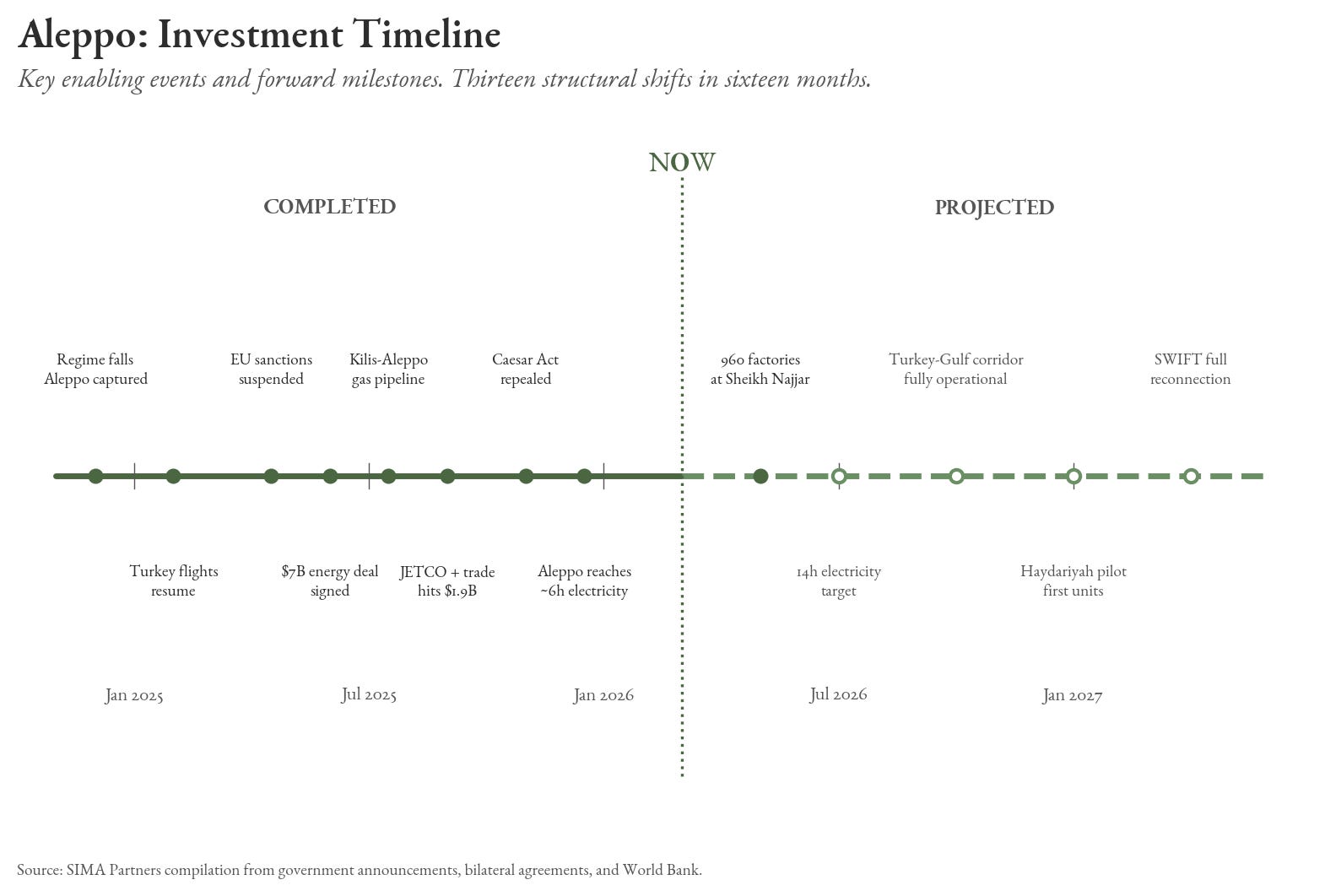

The sixteen months between November 2024 and March 2026 altered the structural conditions for investment in Aleppo more profoundly than the preceding thirteen years combined, even as the broader region remains volatile and the ongoing conflict involving Iran introduces uncertainty that no city-level analysis can fully account for. The velocity of change within Syria is nonetheless part of the investment case, because it suggests that the enabling environment is not slowly improving but rapidly transforming in ways that reward early positioning.

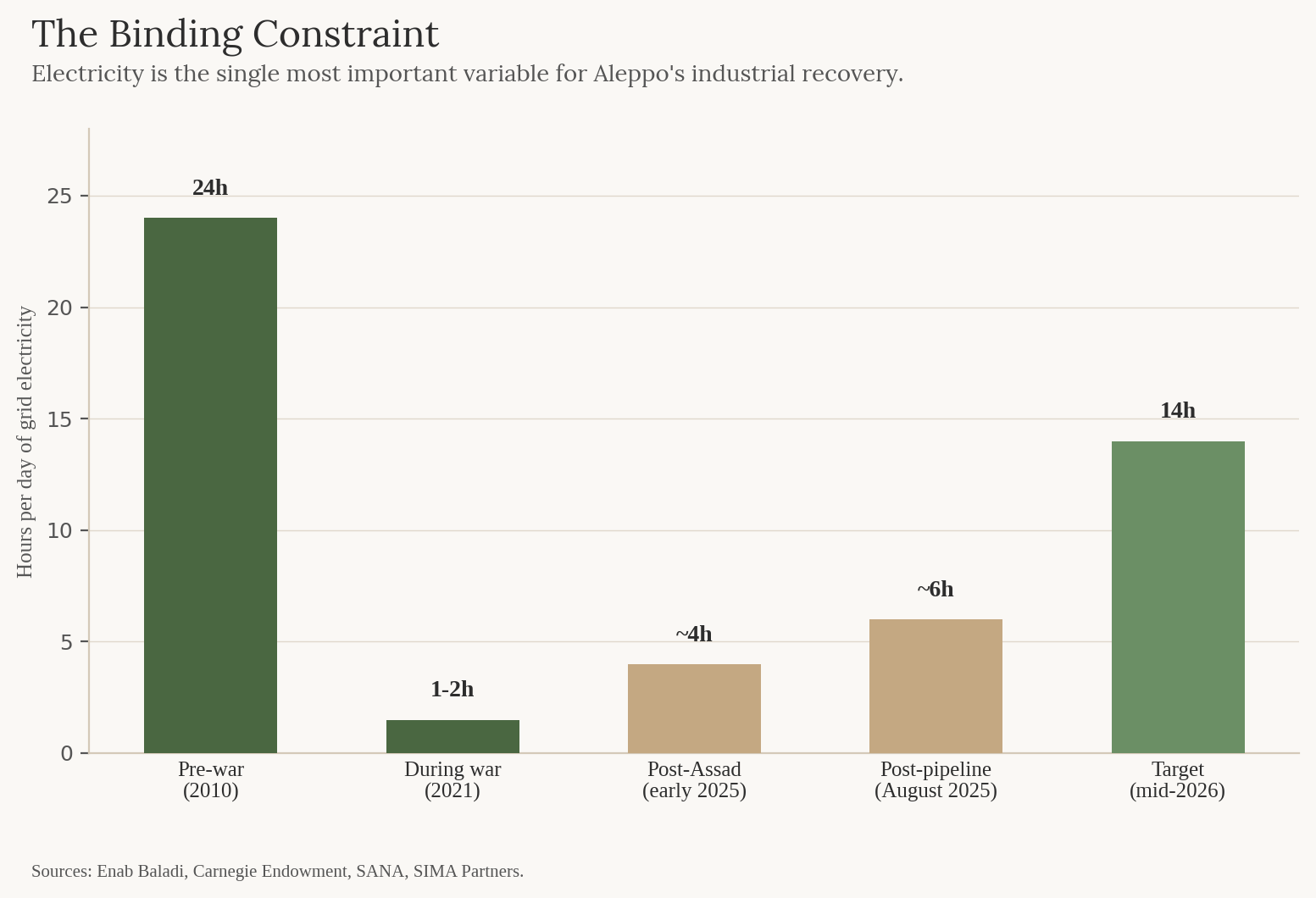

Energy is the variable that matters most for industrial investors: it determines whether Aleppo’s surviving factories can operate competitively or remain economically stranded despite being physically intact. Before the war, Aleppo had 24-hour grid electricity, but by 2021 the city received roughly one to two hours of power for every ten hours of rationing, a level so low that even basic refrigeration was impossible without private generators costing multiples of the average monthly wage. By early 2025, supply had crept to approximately four hours per day, but the activation of the Kilis-Aleppo natural gas pipeline in August 2025, delivering Azerbaijani gas at up to six million cubic metres per day, pushed supply to approximately six hours, with the government targeting fourteen hours by mid-2026 and a $7 billion energy deal covering 5,000 MW of new generation capacity nationally against a pre-war baseline of 8,500 MW and current output of roughly 2,200 MW.

Six hours of grid power is not enough to run a factory at competitive margins, but the trajectory is unmistakable, and every incremental hour of electricity unlocks a tranche of industrial capacity that was physically intact but economically stranded throughout the war years, and the energy investment being made at the national level is simultaneously creating the conditions for returns at the firm level across textiles, manufacturing, and logistics. What matters for investors is not where the grid stands today but where it is heading, and for the first time since 2011, it is heading decisively upward.

The Gaziantep-Aleppo corridor is Aleppo’s single most differentiated advantage over every other Syrian city. The Aleppo-Damascus-Nasib highway has reopened, restoring overland access from Turkey to the Gulf for the first time since 2012, with daily border crossings surging from approximately 3,000 to as many as 20,000 and Turkey-Syria bilateral trade reaching $1.9 billion in just seven months of 2025, with Turkish exports up 54% year-on-year and machinery imports up 244%. Turkey and Qatar have jointly committed $14 billion in infrastructure development across Syria with emphasis on energy and transportation, the Turkey-Syria Business Council has signed cooperation agreements with chambers of commerce in Aleppo, Damascus, Latakia, and Hama, and plans are underway for both an industrial free zone near the Turkish border dedicated to Turkish manufacturers and a Gaziantep-Aleppo railway extending through Damascus and Jordan to the Hejaz.

The competitive implications deserve attention: Turkish construction and manufacturing groups are already the most active foreign operators in Aleppo, with 40% of the industrial city’s pre-war tenants having been Turkish-owned, and their early re-entry gives them a structural advantage in relationships, supply chains, and local knowledge that later entrants from the Gulf or Europe will need to account for, while also raising questions about whether the corridor’s development will produce genuine partnership or a more asymmetric relationship in which Aleppo’s manufacturers become subcontractors to Turkish supply chains rather than competitors in their own right.

The sanctions wall collapsed in sequence. The US executive order in June 2025 suspended most Caesar Act sanctions, the EU suspended most sectoral restrictions in May, Congress repealed the Caesar Act entirely in December 2025, Syrian banks have begun reconnecting to SWIFT, and a new Investment Banks Law has been enacted, collectively bringing the compliance barrier that had deterred even risk-tolerant capital to its lowest level since 2011.

The Arithmetic

The World Bank’s October 2025 assessment puts Syria’s total reconstruction cost at $216 billion against a 2024 GDP of approximately $21 billion, yielding a reconstruction-to-GDP ratio of 10:1 that is the widest of any modern post-conflict economy and that means Syria cannot fund its own rebuilding and must attract external capital at unprecedented scale. At 7% annual growth Syria would need roughly thirty years to return to its pre-war trajectory, and even at 10% the process would stretch over two decades. The closest parallel, Mosul, suffered over 90% destruction in its western sectors with an estimated $50 billion in rebuilding costs and 138,000 buildings damaged. Eight years after liberation, despite the reopening of its international airport in July 2025, much of the city’s western sectors remain in ruins and its main hospital destroyed, even with Iraqi oil revenue behind it that Aleppo lacks. The lesson is specific and the failure modes are instructive: Mosul’s reconstruction was dominated by state-led contracting that crowded out private investment, plagued by corruption in the disbursement of allocated funds (the Iraqi government’s own auditors flagged billions in misallocated reconstruction budgets), and hampered by the absence of a regulatory framework that gave private investors legal certainty on ownership and repatriation.

Syria’s transitional government has, at least rhetorically, taken the opposite approach by seeking private capital over aid, enacting an Investment Banks Law, and publishing an investment opportunities list through the Syrian Investment Agency, but whether the institutional follow-through matches the rhetoric remains the central question. The corollary for investors is that early capital captures the gap between historical capacity and current output, a gap that in Aleppo’s case amounts to roughly $92 billion in cumulative lost output since 2010, but only if the enabling environment continues to develop at the pace of the past sixteen months.

This ratio is the thesis, but its realisation depends on which trajectory materialises. In the base case, electricity reaches 10 to 12 hours by late 2026, the Turkey-Gulf corridor becomes fully operational, and early entrants in textiles and logistics generate first revenues within 12 months, though property rights remain unresolved and real estate investment stays structurally constrained. In the upside case, the 14-hour electricity target is met, the Gaziantep-Aleppo railway converts from feasibility to construction, institutional capital follows the Turkish-Qatari commitment, and Aleppo begins to resemble a functioning regional manufacturing hub within three to four years. In the downside case, the political settlement fractures, electricity stalls at six hours, the property rights impasse hardens, and deployed capital is stranded in a market with no exit liquidity, which is broadly what happened in Mosul. The base case is the most probable, and the investors most likely to succeed will be those who prioritise sectors with short payback periods, textiles and logistics in particular, over those requiring long-horizon commitments such as real estate, at least until the political and regulatory environment demonstrates greater durability.

Where the Capital Goes

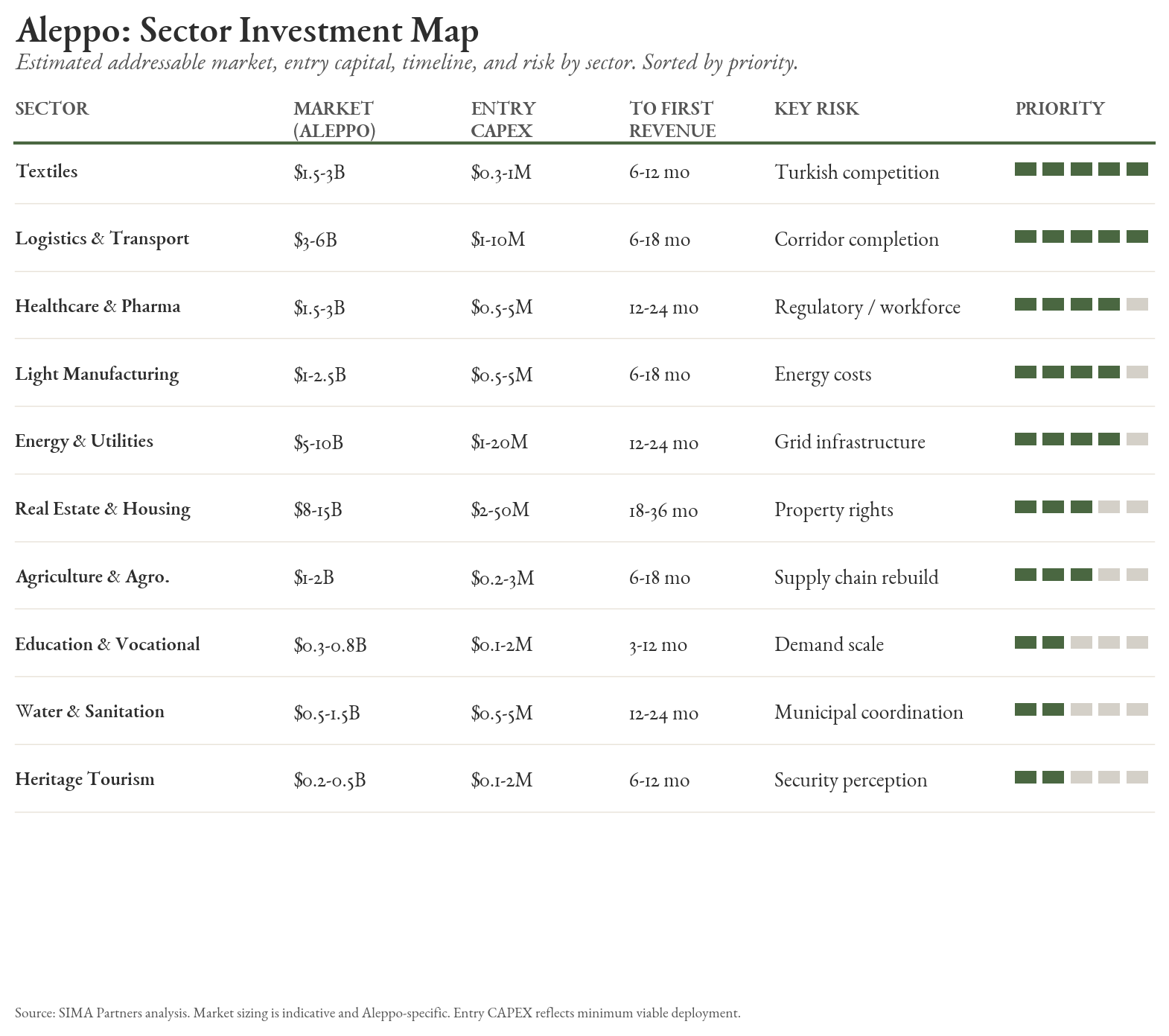

What follows is an assessment of nine sectors against four criteria applied consistently across every city in this series: capital efficiency, near-term feasibility (12 to 24 months), structural demand (permanent versus cyclical), and alignment with Aleppo’s specific comparative advantages. The sector investment map below provides the figures an investment committee needs: estimated addressable market in Aleppo specifically, minimum entry CAPEX, timeline to first revenue, and the binding risk for each sector.

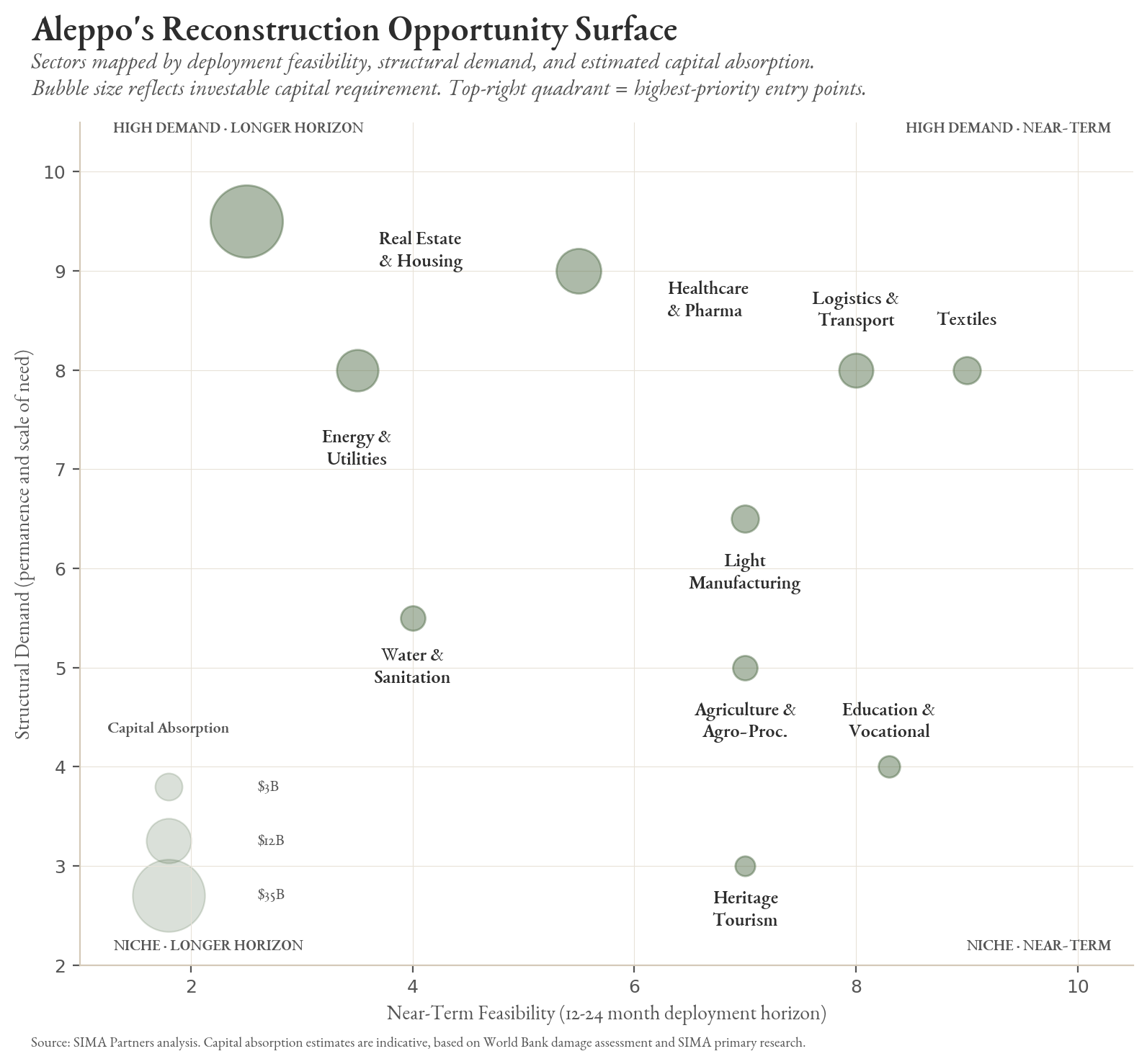

The opportunity surface maps the same sectors along two analytical dimensions, with bubble size reflecting estimated capital absorption, to help investors identify where to concentrate diligence and where to wait.

Textiles are what Aleppo does better than any other city in Syria, and the sector where capital can move fastest because the knowledge never left, it just relocated. The families and workers who built Aleppo’s carpet, garment, and denim industries are still producing in Gaziantep, Bursa, and Egypt, and firms in Aleppo’s industrial zones are already exporting to Iraq, Saudi Arabia, and Lebanon from rehabilitated factory lines, which means the question is not whether Aleppo can produce textiles competitively but whether it can do so at energy costs that match Turkish manufacturers whose lower electricity prices currently give them a significant cost advantage.

Light manufacturing and construction inputs follow a simple logic: Aleppo cannot rebuild itself with imported cement and rebar from Turkey at prices inflated by transport and energy costs, and every housing unit, school, and factory being rehabilitated in the governorate creates demand for locally produced construction materials, plastics, glass, and packaging that the city’s existing industrial shells are well suited to supply, often at deployment timelines shorter than greenfield alternatives because the zoning, road access, and basic infrastructure already exist.

Logistics and transport benefit from a condition that is unique to Aleppo among Syrian cities: the reopening of the Turkey-Gulf overland corridor means that goods moving between 85 million Turkish consumers and the markets of Jordan, Saudi Arabia, and the UAE now pass through or near Aleppo, and the warehouse, cold chain, and freight-forwarding infrastructure needed to service that corridor simply does not exist yet. Early logistics operators face no incumbents, no legacy leases, and a demand curve that rises with every truck that crosses the border.

Healthcare and pharmaceuticals are defined in Aleppo by a specific gap: the city that once housed the majority of Syria’s private pharmaceutical plants and supplied the vast majority of the country’s domestic drug needs now has a returning population of over two million people served by a health infrastructure that was devastated during the war, and the demand for diagnostic imaging, laboratory services, dialysis, and generic medications is not stabilising but growing as families return. That makes this one of the few sectors where the risk of deploying capital is genuinely lower than the risk of waiting.

Energy and utilities in Aleppo present an opportunity not at the generation level, where the $7 billion national consortium deal is already adding capacity, but at the distribution level, because the industrial city’s own administration describes its grid infrastructure as “dilapidated” and industrial consumers in Aleppo currently pay 27 cents per kilowatt-hour compared with 8 cents in Turkey and 5 cents in Egypt, which means any investor who can deliver cheaper, more reliable power to Aleppo’s factories through solar, battery storage, or grid rehabilitation has an immediate and quantifiable market.

Real estate and housing in Aleppo face an unusual combination of overwhelming demand and a structural barrier that prevents capital from entering: eastern Aleppo is largely uninhabitable, the returning population needs housing at a scale the city cannot currently provide, but wartime displacement, regime-era expropriation, and destroyed land registries have created overlapping property claims that make title verification nearly impossible in most neighbourhoods, which is why the Haydariyah pilot on municipally-owned land matters so much as a test case for whether reconstruction capital can flow into housing without being trapped by unresolved ownership disputes.

Agriculture and agro-processing in Aleppo benefit from a resource advantage that no other Syrian governorate can match: the only river basin in the country with excess water supply, which supports olive groves, pistachio orchards, cotton fields, and wheat production that historically accounted for roughly 13% of national agricultural output and that could be connected to export markets through processing facilities (olive pressing, pistachio packaging for Gulf buyers, cotton ginning to feed the reviving textile sector) and cold storage infrastructure linking Aleppo’s farms to Latakia’s Mediterranean port two hundred kilometres to the west.

Education and vocational training matter in Aleppo for a reason that connects to every other sector in this analysis depends on a workforce that does not yet fully exist in the city: returning workers in Aleppo’s industrial zones often lack the technical certifications that export markets require, and the schools and training centres that would produce welders, electricians, CNC machinists, and Turkish-speaking commercial staff were themselves damaged during the war, and demand for private education and vocational programmes is accordingly not a standalone opportunity but an enabling condition for industrial recovery.

Heritage tourism and hospitality are small in absolute terms but carry outsized symbolic and economic weight in a city whose identity is inseparable from its medieval souk and Citadel, and the early signs of revival are visible. The Citadel draws 5,000 weekend visitors since reopening in September 2025, the Aga Khan Trust for Culture has restored 277 shops across eight sections of the souk, and Hisham Jbeili, a sixth-generation Aleppo soap maker, has resumed production in his restored workshop at one-fiftieth of his pre-war capacity, a detail that captures both the resilience and the distance still to travel.

What Can Go Wrong

Political fragility remains the dominant risk, because Syria’s parliament has not been fully formed, there is no ratified constitution, periodic clashes in Aleppo’s northwest underscore that the monopoly on violence is incomplete, and the political settlement, only sixteen months old, has not yet demonstrated the durability long-horizon capital requires.

Property rights constitute the single most consequential risk for physical-asset investment, because wartime displacement, regime-era expropriation laws, destroyed land registries, and decades of informal settlement have created overlapping claims that no court system is currently equipped to adjudicate.

Infrastructure constrains competitiveness: current grid supply is not enough to match regional production costs, and factories face being undercut by Turkish imports priced 30 to 40% below local production because of energy cost differentials that will persist until capacity catches up.

Human capital is the sleeper risk that appears in no damage assessment: average salaries sit at roughly $120 per month, and the skilled diaspora will not return without credible guarantees on security, property, and opportunity that do not yet exist.

Regional conflict casts a shadow over every assumption in this analysis: the ongoing war involving Iran has closed or restricted airspace across the Middle East, disrupted shipping and logistics corridors, and introduced a level of regional instability that could spill into Syria at any point, affecting investor confidence, supply chains, and the physical security of assets on the ground regardless of how favourably domestic conditions develop

.

The Thesis

Aleppo is not a safe bet by any conventional measure, because grid electricity runs six hours a day, property rights are unresolved, the political order that emerged from the December 2024 transition has not yet demonstrated the institutional durability that long-horizon capital demands, and the nearest precedent, Mosul, remains largely unrecovered nearly a decade after its own liberation despite having oil revenue that Aleppo lacks.

It is also a city where 960 factories are running at Sheikh Najjar, where a gas pipeline delivers six million cubic metres a day, where the overland corridor to the Gulf is reopening after thirteen years, where a Turkish-Qatari consortium has committed $14 billion in infrastructure, where sanctions have been lifted, and where the government has told investors at FII Riyadh that it wants reconstruction financed through investment rather than aid.

The 960 factories are the most important number in this analysis, not because of their output, which remains a fraction of pre-war levels and in many cases serves domestic markets at margins that would not yet survive full regional competition, but because of what they represent: a revealed preference by people with their own capital at risk who assessed the damage, weighed the alternatives, and decided that the economics of operating in Aleppo, however constrained, made the bet worthwhile. In April 2025, a delegation of prominent Aleppo industrialists visited Syria for the first time in over a decade, met President Al-Sharaa and toured the industrial city, and sent what the Syria Report described as “a positive signal about potential economic revitalisation,” though they remained cautious and did not announce new investment.

They are not waiting for the risk to resolve; they are the risk resolving, and that distinction matters more than any number in this analysis.

The war destroyed the factories and scattered the families, but it did not move the city, and that is the fact that should anchor every investment thesis written about Aleppo in the years ahead. The economics of geography do not forget, and every century has produced a reason to write this city off, from the Mongol sack to the Ottoman restructuring to the loss of its port to the drawing of borders it never chose, and every century has been wrong, because the logic that made Aleppo a commercial capital for five thousand years was never about the buildings or the institutions or the particular families who happened to hold the leases at any given moment but about the coordinates themselves, about what happens when overland trade routes from the Mediterranean, Anatolia, and the Arabian Peninsula converge on a single point and someone is there to finance, manufacture, and ship what passes through. The reconstruction now underway is not a recovery in the conventional sense but rather the reassertion of that underlying geographic logic after its longest and most violent interruption, and the capital that recognises this earliest will be positioned not merely for the returns of a post-conflict rebound, which are significant but finite, but for participation in the re-emergence of one of the oldest and most durable commercial platforms in the world, a platform whose productive life predates every modern nation-state in the region and whose competitive advantages are embedded not in any policy or institution but in the physical geography of the eastern Mediterranean itself. That is the reconstruction dividend, and the window in which to capture it will not stay open forever.