Damascus: The Capital Reconstructs

There is a useful way to think about Damascus, and it is different from the way you should think about Aleppo, which was the subject of the first briefing in this series and which presents as an industrial reconstruction, a factory floor being reassembled by the families who built it. Damascus is not a factory floor, Damascus is an operating system: the administrative, financial, and institutional architecture through which a country of approximately 22 million people is governed, taxed, educated, medicated, insured, and connected to the outside world. If the capital does not work, nothing else works, and the capital does not work yet.

The city that held this role before 2011 was the seat of a $67.5 billion economy, home to 2.5 million people in the city proper, anchoring a metropolitan area of over five million, housing every government ministry, the Central Bank, Syria’s only stock exchange, and the operational centre of the country’s financial system. Services generated over 43 percent of national GDP, the vast majority intermediated through Damascus: cross-border banking, trade finance, government procurement, import licensing, and the regulatory functions that determined who could do business and on what terms. Government was not an industry in Damascus the way textiles were an industry in Aleppo; government was the city itself, and the capital’s comparative advantage was always institutional rather than industrial.

But this economy was also the product of a specific political arrangement between the city and the state, and that arrangement is now gone. The city’s great trading families had operated the commercial life of the capital for centuries, outlasting the Ottomans and the French, maintaining a merchant culture whose civic pride was visible in the physical fabric of the city: the wide French-mandate boulevards, the Barada river, the jasmine climbing the walls of courtyard houses in Bab Touma and Shaghour, the Ghouta orchards that ringed the city in green.

The first blow to this class came during Syria’s union with Egypt under Nasser (1958-1961), when the United Arab Republic imposed land reform laws that struck at the bourgeoisie’s rural holdings. After the Ba’ath seized power in 1963, the nationalisations of 1963 and 1965 finished the job, liquidating or seriously diminishing the economic power of the merchant and industrial class that had run the city’s commercial life for generations. The exodus hollowed out Damascus’s commercial capacity for a generation, but the capital and talent that left did not disappear: it activated the economies of the countries that received it. The Azhari family founded what became Bloom Bank, now one of Lebanon’s most prominent financial institutions. Across Beirut, Amman, and the Gulf, Damascus’s displaced merchant class seeded business networks, trading houses, and financial institutions that still operate today, and Damascus’s loss was the region’s gain, and whether that capital returns or remains abroad is the question at the centre of the reconstruction thesis.

The merchant class that survived reached an accommodation with the Assad regime in the 1970s: they would not challenge the regime’s political monopoly and the regime would allow them to operate commercially. For a period it held. But the regime did not honour the arrangement, and what followed was a slow displacement in which rural families connected to the security apparatus moved into the city, the commercial networks were progressively captured by regime-connected operators, and the liberalisation of the 2000s, presented internationally as economic reform, in practice awarded the most valuable concessions to a narrow circle of insiders, above all Rami Makhlouf, whose Syriatel monopoly and sprawling business empire came to symbolise a model of crony capitalism in which the state actively structured the private sector to enrich regime insiders at the expense of the productive economy. The old trading families were not destroyed, but they were subordinated, and the civic compact that had maintained the city’s infrastructure and public spaces frayed visibly as the roads deteriorated, the greenery thinned, and the Barada, diverted upstream, ran dry through the city centre, and the most beautiful city in the Levant was degrading not from conflict but from the neglect of people who had no stake in its beauty, only in its control, and the war did not fall on a thriving city but on a city that was already losing itself.

This history is not colour. Damascus has experienced capital flight before, the consequences lasted decades, and the current moment represents the structural reverse: a potential return of comparable magnitude driven by sanctions relief, regime change, and international re-engagement. Whether it materialises depends on whether the new government establishes a new compact with the city. There are early signals: the Syrian Investment Authority, a sovereign wealth fund, a new arbitration body, an Investment Banks Law, SWIFT reconnection. The institutional plumbing is being assembled. But what investors need is not announcements but results: courts that adjudicate predictably, regulatory approvals that move at the speed of business, a demonstrated willingness to let the private sector lead. If the returning diaspora families thrive, foreign capital follows. If they encounter the same apparatus of extraction that operated under Assad, the window closes. Capital remembers.

What Was Lost

The damage to Damascus is geographically asymmetric in a way that has no parallel in the other cities in this series. Central Damascus, the city that most of the world pictures when it hears the name, survived the war almost entirely intact: the Old City with its Umayyad Mosque and Roman colonnades, the western residential districts of Mazzeh and Malki, the commercial centres of Kafr Souseh and Abu Rummaneh, the government buildings and universities. The institutional skeleton of the capital is still standing. Life in central Damascus during the war was degraded, strained, impoverished, but it continued.

A few kilometres away, in the outer ring, it did not. The devastation concentrated in a crescent of eastern and southern suburbs that formed the war’s frontlines from 2012 onward: Jobar, Qaboun, Barzeh, Daraya, Moadamiyeh, Yarmouk Camp, Hajar al-Aswad, and the Eastern Ghouta towns of Douma, Harasta, Irbin, Zamalka, and Ain Tarma. These neighbourhoods, home to over a million people before the war, absorbed years of aerial bombardment, barrel bombs, siege, and chemical weapons, and are now rubble, and the cruelty of the geography is that a few kilometres separated life from death, normality from annihilation, a functioning cafe from a neighbourhood in which the buildings & its inhabitants no longer exist.

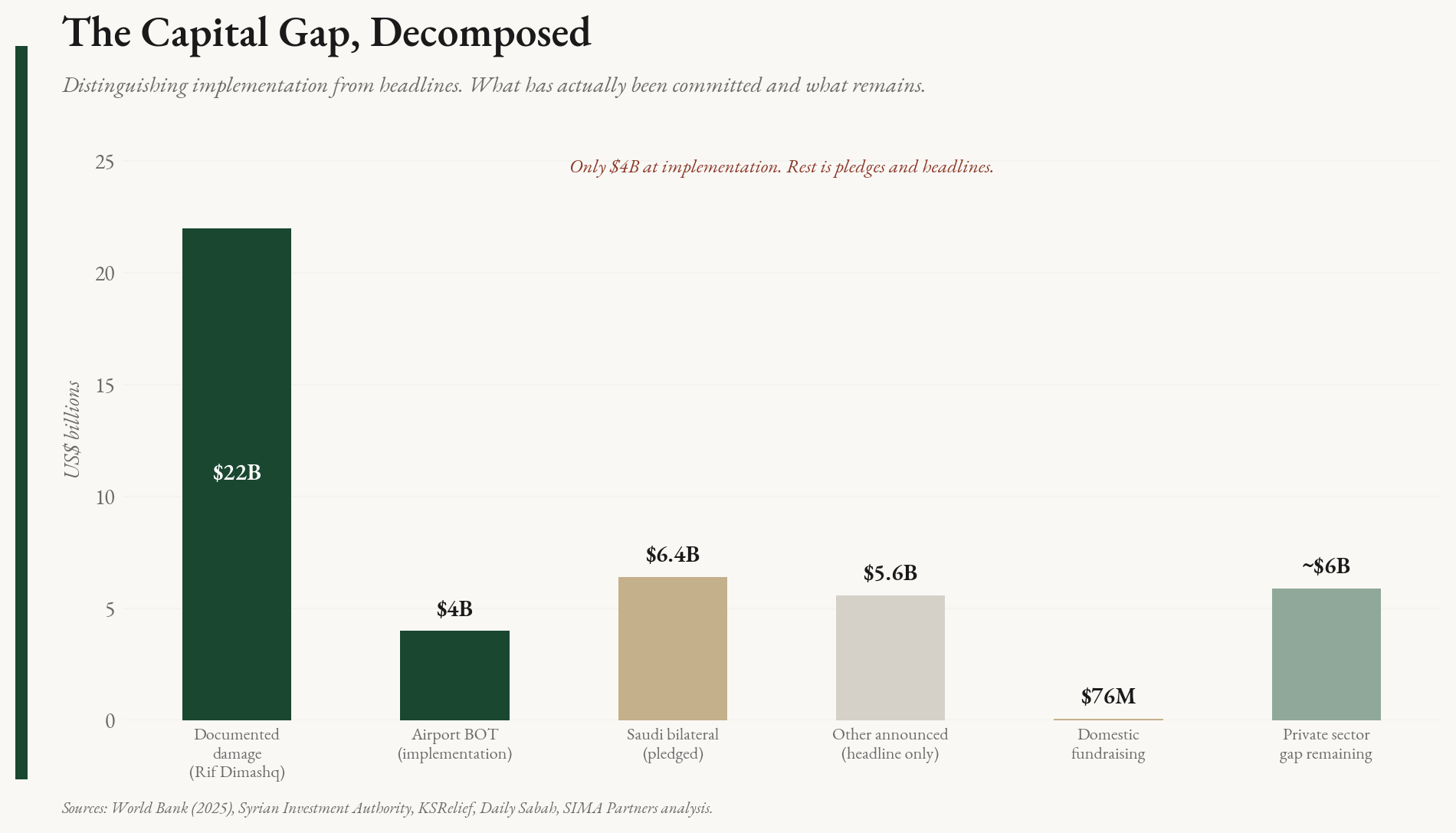

In Jobar, the UN estimated 93 percent of structures devastated by 2018, and the neighbourhood is not damaged but gone, with kilometres of wartime tunnels honeycombing the subsoil whose locations cannot be determined without engineering studies. Mohammed Awata of the Jobar Municipal Board confirmed the tunnels pose a barrier to return, extending deep underground, some containing war remnants that require military cooperation to clear. Mamoun al-Sherawi, who returned from Jordan after the fall, spent an entire day walking through Jobar identifying the ruins of his home by memory; he found it, and it needed to be rebuilt, not repaired. UNITAR satellite assessments documented 34,136 affected buildings in Eastern Ghouta alone, and the World Bank’s October 2025 assessment placed Rif Dimashq as the second most damaged governorate after Aleppo, with $22 billion in estimated direct physical damage out of $108 billion nationally.

But the damage the World Bank does not count is the damage that matters most. The electricity grid has improved from two hours daily to roughly eight, with the government targeting fourteen hours by mid-2026. Only a third of the country has internet access. The Syrian pound has lost 99.5 percent of its value. 1.5 million people were displaced from greater Damascus, taking a generation of professional capacity with them. The government ministries that physically survived are inhabited by two governments at once: new leadership at the top, thousands of Assad-era civil servants at every operational level, and a foreign investor walking into a ministry today encounters not a reformed institution but a layered one, new appointees and old bureaucrats in mutual incomprehension, every approval slowed to a pace functionally indistinguishable from obstruction.

What remains is a city whose skeleton stands but whose connective tissue has been deeply eroded, and yet a 100-square-metre retail unit on a main commercial street commands approximately $250,000 per year, a figure remarkable for a capital where the banking system barely functions, and what it tells you is that the market is pricing in the reconstruction ahead of the infrastructure, concentrating demand in the narrow band that survived while the destruction belt remains locked.

What Changed

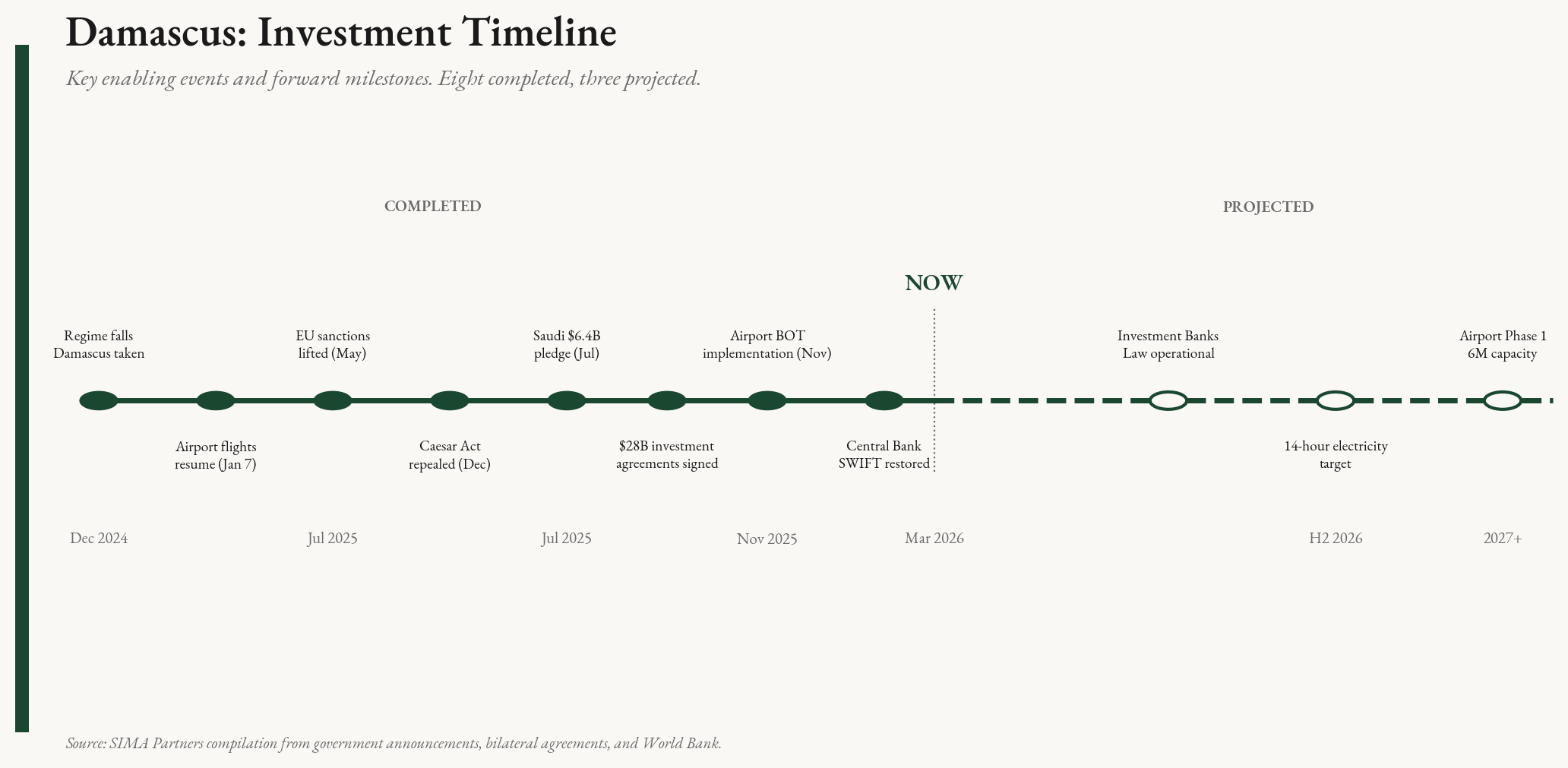

Three shifts redraw the map: sanctions broadly lifted, international flights resumed from Damascus International Airport on January 7, 2025, and the transitional government signaled that reconstruction would be financed through private capital. The capital is open for the first time in over a decade.

The transitional government under Ahmed al-Sharaa adopted an explicit strategy of reconstruction through private investment, not aid or sovereign borrowing, and in ten months signed $28 billion in investment agreements. The most significant is a $4 billion BOT to rebuild Damascus International Airport, signed with a consortium led by Qatar’s UCC Holding, with defined concession terms, an experienced operator group (Kalyon and Cengiz delivered Istanbul Airport in 42 months), implementation-phase contracts signed November 2025, Terminal 2 under construction, and a masterplan by Zaha Hadid Architects. Saudi Arabia pledged $6.4 billion in bilateral deals including rubble clearance, water rehabilitation, and reconstruction of 34 schools. Other announced commitments, a $2 billion UAE-backed metro and a $2 billion towers project with Italy’s UBAKO, remain opaque: counterparties unclear, concession structures unpublished, no implementation timeline disclosed, and the gap between the announcement and the execution is where investors must exercise the most discipline.

The new Investment Law (Decree 114) establishes a Syrian Investment Authority affiliated with the president, grants foreign investors 100 percent ownership and full profit repatriation, and offers permanent tax exemptions in priority sectors including pharmaceuticals, agriculture, and export-oriented manufacturing. SIMA Insights analysed the SIA framework in detail separately, noting both the ambition and the long-term fiscal risks of incentives without sunset clauses.

The third shift concerns land, and it is the one that will determine whether the first two matter. The destroyed suburbs included substantial areas of informal housing where ownership was established by occupancy rather than title deed, and the old regime weaponised this ambiguity through Decree 66 (2012) and Law 10 (2018), which created legal mechanisms to rezone destroyed areas and transfer development rights to regime-connected investors. Marota City, a luxury development on 2.14 million square metres of southwest Damascus built over the razed Basateen al-Razi neighbourhood, is the result: 7,500 families displaced, fewer than ten percent rehoused.

The Arithmetic

The numbers that reveal Damascus are not the national aggregates but the ones that describe the capital’s financial infrastructure before the war and its absence after it.

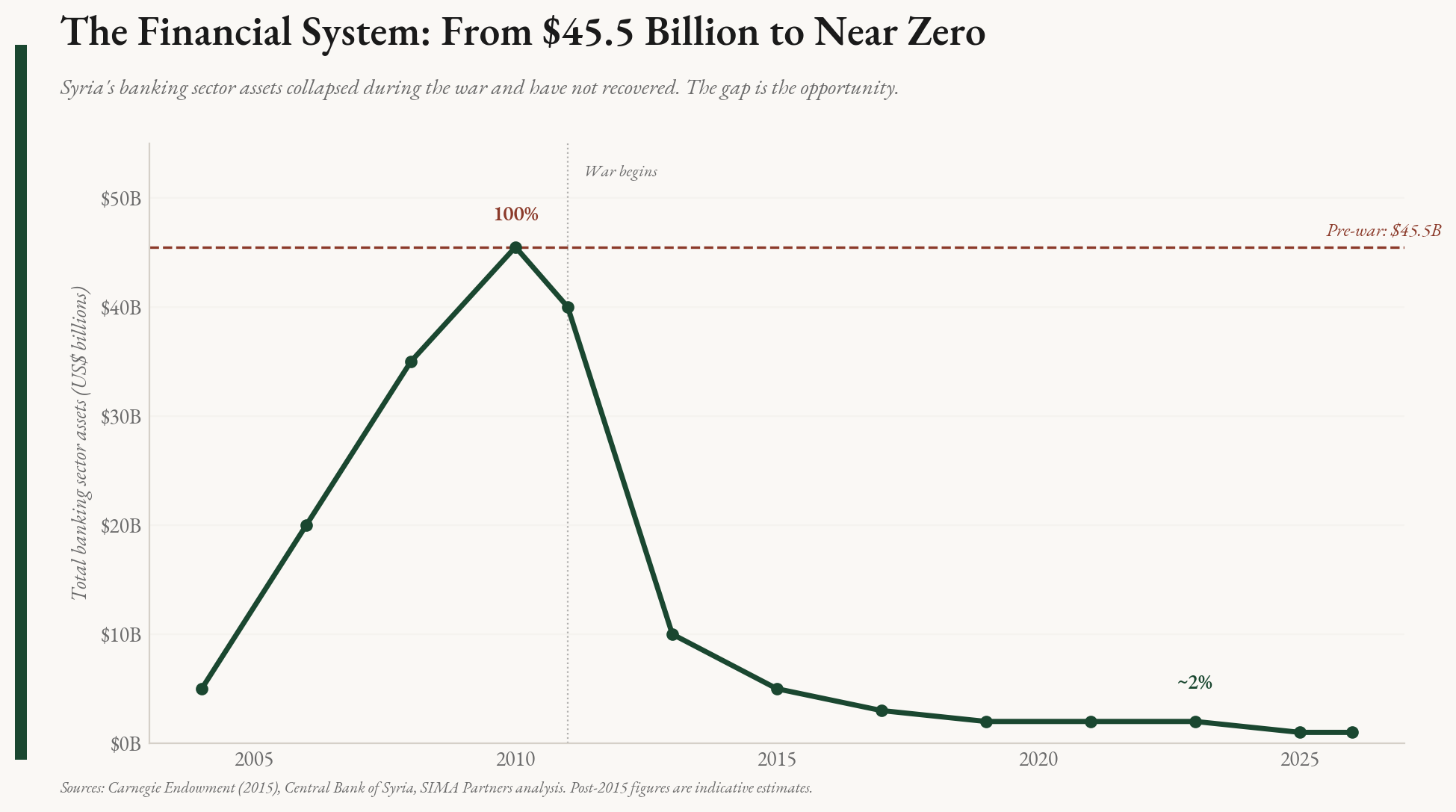

By 2010, Syria had 14 private banks with $45.5 billion in total sector assets, almost all headquartered in Damascus, but even then the country was radically underbanked: 41,600 people per bank branch against Lebanon’s 4,700, loans-to-GDP of 45 percent against Lebanon’s 101 percent, insurance penetration of 0.62 percent of GDP against a global average of 6.6 percent, a stock exchange trading $5 million per week against Amman’s $16 million per day. What was underdeveloped before the war has since been destroyed entirely, and the distance between where Damascus stood and where it needs to be is not a gap but a void, one that represents simultaneously the scale of the reconstruction challenge and the scale of the greenfield opportunity.

The metropolitan area is rebounding toward five million, growing at 4.35 percent annually on returning refugees. Of the $28 billion in investment agreements signed nationally, approximately $10 billion is Damascus-area specific, and of that, only the airport has moved to implementation. The government will not borrow, multilateral donors are not arriving at scale, and private capital is the only mechanism.

Where the Capital Goes

Damascus’s reconstruction is not a list of parallel sectors but a dependency chain: each link enables the next, and capital deployed out of sequence gets stranded. The chain runs from institutional infrastructure through connectivity, energy, and finance to the physical reconstruction that absorbs the largest sums but sits furthest downstream, and every investor must decide where in that chain to enter.

Institutional modernisation is the binding constraint on every other sector in this analysis, and it is itself an investable category. Damascus cannot absorb $216 billion in reconstruction capital through ministries that run on paper, process approvals manually, maintain no digital land registry, and require physical presence for every interaction. E-government platforms, digital permitting and licensing systems, regulatory process automation, land registry digitisation, and English-language capacity building for the civil service are not reforms that happen after the reconstruction succeeds; they are the preconditions without which the reconstruction does not begin. Countries that rebuilt at speed, from Rwanda to Georgia to the UAE, did so because they built the institutional machinery first. The opportunity is real and immediate: international development firms, govtech companies, and institutional advisory practices can deploy into Damascus now, working with ministries that are willing but lack the tools, the frameworks, and the trained personnel to operate at the speed the reconstruction demands. Estimated addressable market: $50-200 million over five years across e-government, digital registries, capacity building, and regulatory design. Minimum entry CAPEX: $200K-$5 million. Timeline: 3-12 months to first engagement. Binding risk: political will to implement, since institutional reform creates losers among those who benefit from the current opacity.

Aviation and connectivity is the second link, because Damascus International Airport is both a standalone revenue-generating infrastructure asset and the physical prerequisite for everything that follows: no functioning airport, no tourism recovery, no business travel, no diaspora reconnection, no cargo logistics at scale. The $4 billion BOT is the lowest-risk major project in Syria, with defined concession terms, operators who delivered Istanbul Airport, and construction underway. Estimated addressable market: 6 million passengers by end-2026 ramping to 31 million at full build-out. Binding risk: regional airspace disruption from the Iran-Israel conflict.

But planes landing at a functional airport deliver passengers into a city that cannot reliably keep the lights on, which is why energy is the third link and the constraint on every commercial sector. Grid supply has quadrupled since the transition, but the $7 billion national energy deal targets 12 GW by 2030 against current output that remains a fraction of that, with over 50 percent of transmission infrastructure damaged or decayed. The near-term opportunity is not generation at scale but decentralised solutions: solar, battery storage, grid-edge systems for commercial and residential consumers paying diesel-generator premiums that make distributed alternatives immediately competitive. Estimated addressable market in the Damascus metro: $200-400 million over five years. Minimum entry CAPEX: $500K-$2 million. Timeline: 6-12 months to first revenue. Binding risk: regulatory uncertainty on grid interconnection and tariff structure.

Financial services, without which a $216 billion reconstruction cannot be intermediated, you cannot rebuild a country through a cash economy. The Central Bank under Governor al-Husrieh is reconnecting to SWIFT, the Investment Banks Law has been enacted, the Damascus Securities Exchange barely transacts. Payments, credit, insurance, trade finance, mobile money: all greenfield, and the institutions licensed now will be the institutions through which every subsequent dollar of reconstruction capital flows. Estimated addressable market: the entirety of Syria’s formal financial intermediation, which currently approximates zero. Entry CAPEX: $2-10 million for a payments platform, $10-50 million for an investment bank. Timeline: 12-24 months to operational. Binding risk: regulatory framework still being written; Central Bank independence uncertain.

With power and payments functioning, construction and commercial real estate become the fifth link, and this is where the thesis becomes physical. Damascus cannot serve as the capital of a $216 billion reconstruction if there is nowhere for the people doing the reconstruction to work, meet, stay, and operate. The city needs hotels that can host the investor delegations, government delegations, and international organisations that are already arriving and finding a city without adequate accommodation. It needs Grade A office space where advisory firms, law firms, and corporate regional headquarters can establish permanent presence. It needs commercial developments in the surviving core, on land with clear title, serving demand that already exists and is growing with every flight that lands and every family that returns. Decree 114 provides the legal framework, and the demand is visible in the $250,000-per-year retail rents that the market is already commanding in the core. Estimated addressable market: $500 million to $2 billion over five years in the Damascus metro. Minimum entry CAPEX: $5-50 million. Timeline: 12-24 months. Binding risk: commercial rents deterring the investors the city needs, and construction costs inflated by energy and import dependence.

Healthcare requires every link above it in the chain, stable power and functioning payment systems, which is why it sits here rather than higher. But the demand is immediate and growing: the Ministry of Health has set targets for out-of-pocket spending reduction from 45 to 40 percent by 2030, insurance coverage of 1.6 million by 2028, and DHIS-II digital health deployment across the public system. Private diagnostic and specialty care serves a rebounding metropolitan population with limited alternatives. Estimated addressable market: $500-$700 million over five years. Minimum entry CAPEX: $600K-$5 million per facility. Timeline: 9-15 months. Binding risk: clinical workforce availability; brain drain has not reversed.

Education and vocational training may be the most underestimated link, because every other sector depends on a workforce that does not exist at scale, the gap widens with every deal signed, and the demand is already visible in the inability of returning businesses to find qualified staff. Syria before 2011 produced engineers, doctors, and administrators for the region. That capacity has been decimated, and without it the entire chain decelerates. Estimated addressable market: $300 million to $1 billion over five years. Minimum entry CAPEX: $200K-$5 million. Timeline: 3-12 months. Binding risk: circular, since without the workforce the other sectors cannot accelerate.

The destruction belt is a fundamentally different category from the construction opportunity above. The commercial real estate in the surviving core can proceed on clear title; the periphery cannot. Five million people need housing; demand is not the constraint. The constraint is legal: wartime displacement, regime-era expropriation laws, destroyed land registries, and decades of informal settlement have created overlapping claims that no court system is currently equipped to adjudicate.

But the scale of destruction also creates an opportunity that does not exist in the surviving core: the chance to build from zero. The eastern and southern suburbs were severely unplanned, and underserviced before the war. Rebuilding them to the same standard would be a failure of imagination. The destruction belt is where Damascus can deploy affordable housing at scale, planned communities with embedded solar, fibre, water recycling, and digital municipal systems that the surviving core will spend decades retrofitting. Countries that rebuilt after large-scale destruction did not replicate what existed; they leapfrogged it. Estimated addressable market: $10-15 billion over a decade. Minimum entry CAPEX: $10-100 million per development phase. Timeline: 24-60 months, contingent on property-rights resolution. Binding risk: property-rights gridlock, and no amount of master planning substitutes for legal clarity on who owns the land.

What Can Go Wrong

Geopolitical and political risk remain present but are evolving in directions that favour the thesis. The transitional government is sixteen months old, there is no ratified constitution, and the political settlement has not yet demonstrated the durability that long-horizon capital requires. The regional war involving Iran introduces instability that could spill into Syria at any point. But the trajectory of international re-engagement is unmistakable: as this briefing goes to publication, President al-Sharaa is completing his first official visits to Germany and the United Kingdom, meeting Chancellor Merz and Prime Minister Starmer, discussing reconstruction, economic cooperation, Syria’s reintegration into the international financial system, and the return of skilled diaspora professionals. France received al-Sharaa in May 2025. The SIA chairman visited London & Paris last week to meet construction firms and financial institutions. The signals from European capitals, coming amid regional volatility, suggest that the international community has decided that engaging with the Syrian project is preferable to waiting for perfect conditions, and investors would do well to read that signal carefully.

Commercial real estate pricing has become an obstacle in its own right: the concentration of demand in the surviving core has pushed rents to levels that deter the investors the reconstruction needs, and the risk over the next three to five years is that prices in the core spiral while the periphery remains stalled, leaving a city that is simultaneously unaffordable where it functions and uninvestable where it does not.

The bureaucracy is not a background risk; it is the risk.

Through our work on the ground in Damascus, we can confirm that the new government’s intentions are genuine and authentic, but intentions do not process investment licences, and the devil is in the execution. Tens of thousands of Assad-era civil servants remain embedded in every economic ministry, operating on paper-based systems, applying procedures designed not for speed but for control, and the danger is not that the old regime persists in ideology but that it persists in method: the same opaque, access-driven structures, the same ministerial gatekeeping, the same pace that functionally cannot distinguish between caution and obstruction, with different people sitting at the top. International investors see through this immediately, and so do the compliance teams at every bank considering SWIFT reconnection. Whether the transitional government extends the institutional reset it applied to Defence, Foreign Affairs, and Interior to the economic ministries, and does so with urgency, is the single most important leading indicator investors should watch, because the speed of reconstruction will move at exactly the speed of bureaucratic reform, and no faster.

Human capital and macro fragility compound each other: the skilled professionals who left have not returned in significant numbers and will not return without credible guarantees on security, property, and opportunity, while the economy grows at roughly one percent, Turkish imports surge 60 percent as Syrian exports halve, 41 percent US tariffs apply to Syrian goods, and the economy is being liberalised faster than institutions are being built to manage the consequences.

The Parallel

The parallel is Beirut after 1990, where the Solidere model consolidated property over destroyed central Beirut, attracted Gulf capital, rebuilt a commercial district, and delivered physical reconstruction that failed at everything else: the legal structure severed the connection between original owners and the rebuilt district, converting property rights into shares that most holders sold at a fraction of market value, which destroyed the organic demand base and left a downtown that was physically spectacular and economically empty. The people who would have lived and worked there had been priced out or bought out, and three decades later the rebuilt core exists alongside a collapsed economy and an insolvent banking system.

Marota City is Damascus’s Solidere: same legal structure, same displacement dynamic, same unanswered question. But the analogy has a structural limit: Solidere was one project in one district, whereas Damascus’s reconstruction spans an entire metropolitan periphery, thousands of hectares, dozens of neighbourhoods, millions of beneficiaries, and the Jobar Board of Trustees’ master plan represents something Beirut never produced, a community-driven property framework emerging from the displaced population itself, and if the government builds on it Damascus has a mechanism for distributed reconstruction that Beirut lacked, and if it overrides it Damascus gets Beirut’s outcome at ten times the scale.

The Thesis

There is no capital city in the MENA region simultaneously reopening after total isolation, receiving its first private capital in over a decade, operating with near-zero financial infrastructure, and sitting at the centre of a $216 billion reconstruction. This convergence is a window, not a permanent condition.

But if Aleppo is a factory that needs to be reassembled, Damascus is an institution that needs to reinvent itself, and the distinction matters because factories can be rebuilt with capital alone while institutions cannot. The aspiration for Damascus to become a Singapore or a Dubai is valid, and Syria’s leadership has invoked both models, but those transformations were 25-year commitments built on institutional fundamentals, not on announcements. E-government, anti-corruption enforcement that investors can verify, ease and speed of doing business measured in days, not months, ministries that operate digitally, not on paper. A regulatory environment where approvals move at the speed of capital, not at the speed of a bureaucracy that was designed under Assad to slow things down. These are not reforms that happen after the reconstruction succeeds; they are the preconditions without which the reconstruction does not begin, and the best delivery that President Ahmed Al-Sharaa and the transitional government can make to the world is not another billion-dollar MOU but a functioning ministry that processes an investment licence in thirty days, because that is the signal that changes everything.

Several of Syria’s most prominent commercial families have already returned and begun deploying capital, including the Saids, Challahs, Kashlans, Ghreiwatis, Daabouls, and others. None of them waited for the risk to resolve, they assessed the conditions with their own money at stake and decided that in a state-formation environment, the cost of being late exceeds the cost of being early. Their presence is the signal that matters more than any bilateral agreement announced at a conference, because conferences produce memoranda of understanding and returning families produce leases, payrolls, and commercial activity, which is the difference between an intention and a fact.

The banks being licensed now will be the banks through which reconstruction capital flows for the next twenty years. The regulatory relationships being formed now will determine who gets the permits and who does not. The legal frameworks being drafted now will govern property rights across the destruction belt for a generation. None of this will be done twice.

As this briefing goes to publication, the regional war involving Iran has slowed movement in Damascus. The airport is closed, the security environment has deteriorated in ways that affect daily operations and investor confidence. But the work has not stopped, the companies and families and institutions that are building the architecture of the new Syria are still at their desks, still signing leases, still hiring staff, still preparing for the moment the regional conflict subsides and the window reopens wider than before.

The question is not whether Damascus will be rebuilt but whether it will be reinvented, whether the operating system that governs this country will be rewritten for the century ahead or merely patched. The answer will determine not just whether the reconstruction succeeds but whether the capital becomes worthy of the country it is supposed to lead.